Executive Summary

As traditional fixed-income markets evolve amidst fluctuating interest rates and shifting investor preferences, tokenized private credit emerges as a compelling alternative. Leveraging blockchain technology, this innovative approach transforms private lending by offering enhanced liquidity, transparency, and efficiency. By digitizing real-world assets, investors gain direct access to institutional-grade debt instruments, reshaping strategies within the DeFi fixed income landscape.

Introduction

The financial sector is witnessing a paradigm shift. Traditional fixed-income instruments, while foundational, often grapple with limitations such as illiquidity and opacity. Enter tokenized private credit—a fusion of private lending and blockchain technology—offering a modernized approach to fixed-income investing. This white paper delves into the mechanics, benefits, challenges, and future prospects of this burgeoning sector.

1. Understanding Tokenized Private Credit

Tokenized private credit is a groundbreaking innovation in the world of fixed-income investing. It involves the digitization of private debt instruments—such as loans to small and mid-sized enterprises (SMEs), real estate developers, or infrastructure projects—by converting them into tradable digital tokens using blockchain technology. This process bridges the gap between traditional lending and decentralized finance (DeFi), offering investors access to private credit opportunities that were once the exclusive domain of large institutions, private equity firms, or accredited investors.

At its core, tokenized private credit aims to make private lending more accessible, liquid, and transparent. By leveraging the decentralized and programmable nature of blockchain, this model enables the creation of smart contracts that can automatically manage loan terms, interest payments, amortization schedules, and repayments. As a result, the market for tokenized debt instruments is becoming an increasingly attractive avenue for yield-seeking investors, especially in a macroeconomic environment where traditional fixed-income returns have been constrained by fluctuating interest rates and inflationary pressures.

Key Features of Tokenized Private Credit:

Fractional Ownership

Tokenization allows a single debt instrument—such as a $1 million SME loan—to be divided into hundreds or thousands of digital tokens. Each token represents a proportional ownership share in the loan and its associated cash flows. This fractional ownership model lowers the minimum investment threshold significantly, allowing retail investors and smaller institutions to access high-quality credit opportunities without needing to deploy large amounts of capital.

For example, instead of needing $250,000 to invest in a traditional private credit fund, investors could gain exposure for as little as $500 through tokenized offerings. This democratization of access is attracting interest from digital asset portfolio management firms and crypto investment companies looking to diversify into fixed-income assets while broadening their client base.

Enhanced Liquidity

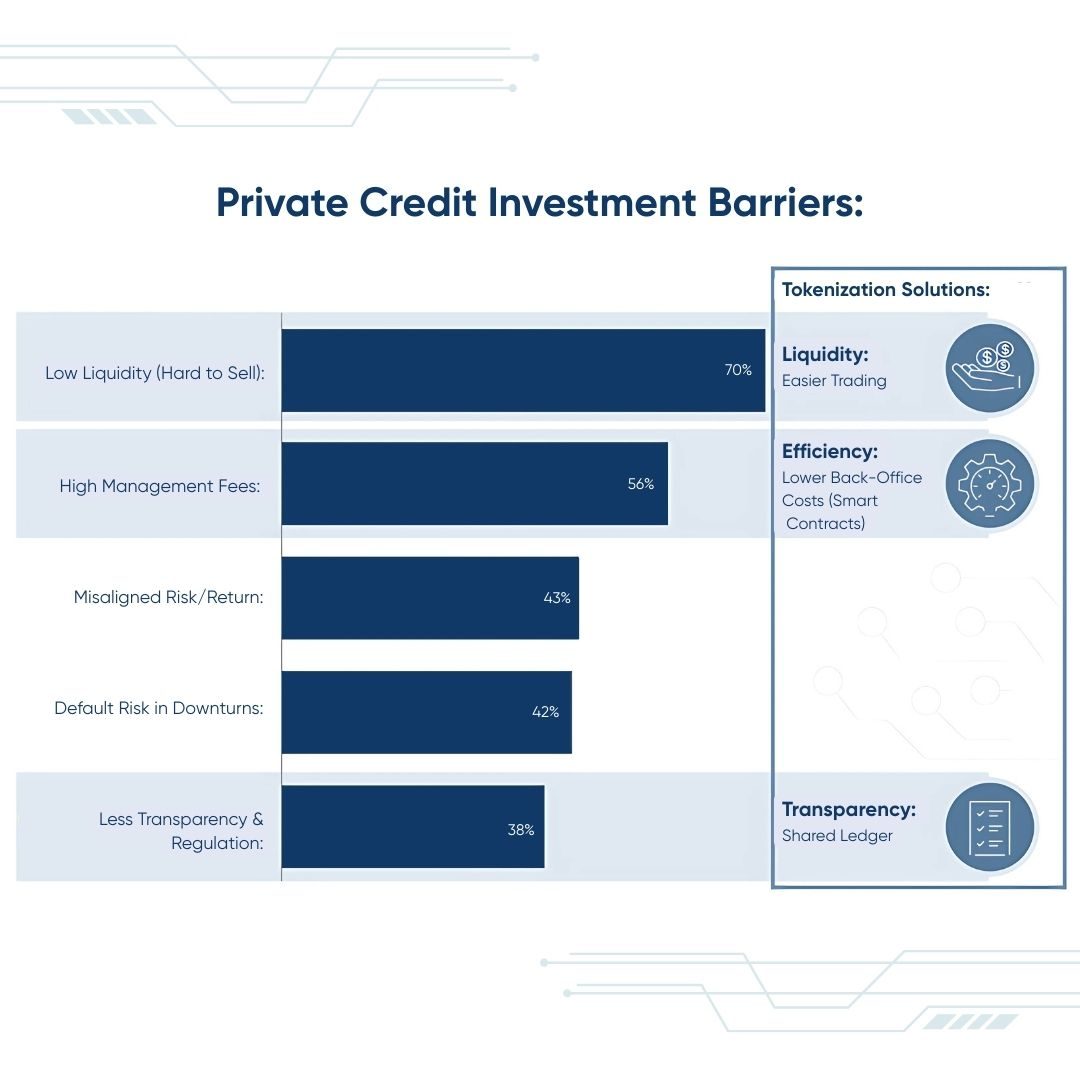

One of the long-standing challenges in private credit markets is the illiquidity of investments. Traditional loans are often held until maturity, with limited or no secondary market activity. Tokenized credit instruments, on the other hand, can be traded on regulated digital asset exchanges or within DeFi liquidity pools, providing investors with the option to exit positions before maturity.

Platforms like Maple Finance and Credix are already facilitating this kind of marketplace, where investors can buy and sell tokenized credit positions. This introduces a secondary market dynamic that historically hasn’t existed for private loans—making it possible to manage liquidity risk more effectively while enhancing portfolio flexibility.

Transparency and Trust

Blockchain’s decentralized and immutable ledger serves as a single source of truth for all transaction records, ensuring transparent documentation of every aspect of the lending process—from loan issuance to interest payments and default tracking. Unlike traditional finance, where access to loan performance data may be delayed or obscured, tokenized private credit allows real-time updates and on-chain verification.

This level of data transparency not only strengthens investor confidence but also enables portfolio management consultants to evaluate and monitor credit risk with greater accuracy. Moreover, smart contracts automatically enforce loan agreements, reducing the possibility of human error or manipulation while ensuring timely repayments and consistent execution.

Real-World Example: Goldfinch

A notable example of tokenized private credit in action is Goldfinch, a DeFi protocol that provides undercollateralized loans to businesses in emerging markets. By sourcing capital from crypto investors and directing it to local lending institutions, Goldfinch helps fund small businesses and infrastructure projects in regions where access to traditional credit is limited.

Each loan issued through Goldfinch is represented by tokens, which investors can purchase to earn yield over time. The project uses smart contracts to handle interest payments and principal repayments, offering a high degree of automation and efficiency. For investors, this presents an opportunity to gain exposure to global credit markets with a diversified, risk-adjusted return profile.

Real-World Example: Tradable on zkSync

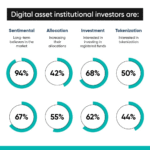

Another innovative approach is offered by Tradable, a firm that has tokenized over $1.7 billion worth of private credit assets on the zkSync blockchain, a Layer 2 solution for Ethereum. By operating on zkSync, Tradable offers faster transaction processing and significantly lower fees, while enabling institutional-grade investors to interact with on-chain private debt markets in a secure and scalable way.

This type of infrastructure is drawing the attention of blockchain asset consulting firms, who are advising clients on how to integrate tokenized private credit into larger digital asset investment strategies.

Tokenized private credit represents a significant shift in how debt is issued, managed, and accessed. By removing the traditional barriers of entry, improving liquidity, and offering real-time transparency, this model provides an innovative alternative for investors seeking fixed-income solutions beyond the limitations of conventional markets. As regulatory frameworks and technological standards continue to evolve, tokenized private credit is poised to become a cornerstone of the next generation of digital asset management services.

2. The Role of Blockchain in Private Lending

Blockchain technology serves as the foundational infrastructure for tokenized private credit, reshaping how private lending is conducted, managed, and scaled. By embedding transparency, automation, and decentralization directly into the lending process, blockchain introduces a new level of efficiency and trust—elements that are critical in the traditionally opaque world of private credit.

In contrast to conventional private lending—where record-keeping is centralized, paperwork-intensive, and prone to inefficiencies—blockchain-based platforms enable seamless data sharing, real-time verification, and tamper-proof audit trails. These innovations open the door for both crypto investment companies and institutional investors to participate in private credit markets with significantly lower operational friction.

Key Blockchain Advantages in Private Lending:

Smart Contracts: Automating the Lending Lifecycle

Smart contracts are self-executing agreements written in code and deployed on a blockchain. In private lending, they can automate a wide array of processes, from loan origination and underwriting to disbursements, repayments, and defaults. This automation minimizes human error, reduces administrative overhead, and ensures that agreements are enforced consistently and transparently.

For instance, in a tokenized lending arrangement, a smart contract might automatically distribute interest payments to token holders based on a predefined schedule. It could also initiate penalties for missed payments or trigger collateral liquidation in the event of default. These smart contracts act as programmable trust agents, enforcing rules without the need for intermediaries or manual oversight.

Platforms such as Maple Finance and Centrifuge leverage smart contracts to facilitate decentralized lending pools, allowing participants to contribute capital to vetted borrowers with built-in risk management protocols. This use of technology aligns with the interests of portfolio management consultants, who seek tools that improve both operational efficiency and investor confidence.

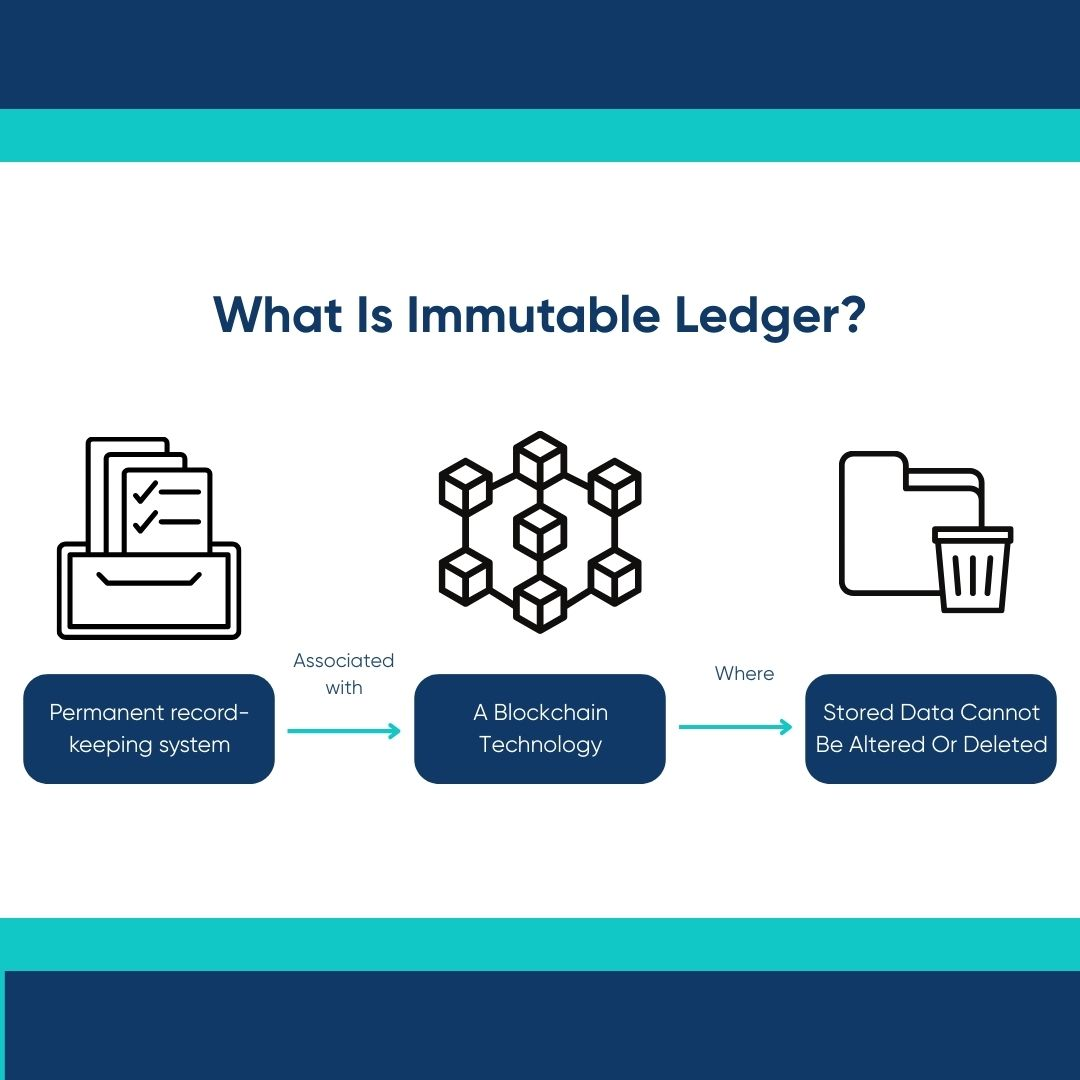

Immutable Records: Ensuring Trust and Auditability

Another fundamental strength of blockchain lies in its immutability—once data is recorded on a blockchain, it cannot be altered or deleted. This feature creates a single, verifiable source of truth for all loan-related transactions, from initial agreements to payment histories.

In traditional private lending, verifying the legitimacy and terms of a loan can require sifting through scattered documentation across various parties, often with limited transparency. With blockchain, every aspect of the loan lifecycle is recorded in real-time, viewable on-chain by all authorized stakeholders. This enhances auditability and regulatory compliance, making it easier for digital asset consulting for compliance professionals to ensure integrity and adherence to applicable standards.

A real-world example can be found in TrueFi, a decentralized protocol that uses blockchain to log credit lines, interest payments, and repayment events. Lenders can view loan histories, borrower reputations, and protocol-level metrics—instantly and transparently. This degree of visibility fosters trust between lenders and borrowers and supports more accurate investment analysis and portfolio management.

Decentralization: Reducing Reliance on Intermediaries

Perhaps the most transformative aspect of blockchain is its decentralized architecture. Traditional private lending involves a network of intermediaries—underwriters, custodians, legal teams, clearinghouses, and fund administrators—each of whom adds time and cost to the process. Blockchain removes the need for many of these middlemen by enabling peer-to-peer financial interactions.

Through decentralized lending protocols, capital can flow directly from lenders to borrowers without passing through banks or fund managers. This reduces fees, accelerates processing times, and increases yield potential for investors. Moreover, borrowers gain more direct access to global liquidity sources—especially useful for SMEs and emerging-market entrepreneurs who may be underserved by conventional finance.

Take Credix, for example—a platform connecting DeFi capital with real-world borrowers in Latin America. By tokenizing off-chain credit opportunities and eliminating the traditional layers of gatekeepers, Credix reduces overhead and unlocks lending opportunities that were previously inaccessible to most investors.

This model also resonates with the goals of RWA tokenization investment consultants, who advocate for broader access to high-yield fixed-income assets through blockchain-based solutions.

Additional Blockchain Benefits in Private Lending:

- Programmability:Terms and conditions can be embedded directly into tokens, such as locking them until a repayment milestone is met, or triggering yield adjustments based on borrower credit scores.

- 24/7 Market Access:Unlike traditional lending systems that operate within banking hours, blockchain-based lending is accessible around the clock, facilitating real-time transactions and global participation.

- Identity and Credit Scoring Innovations: Using decentralized identity systems and on-chain behavioral data, borrowers can build digital credit profiles that travel across platforms—reducing the reliance on outdated or region-specific scoring models.

- Integration with Stablecoins: Tokenized loans can be denominated and paid in stablecoins for investment, enabling seamless cross-border lending and protecting against currency volatility.

How Blockchain Enhances Institutional Confidence

Institutional investors and bitcoin investment consultants are increasingly exploring tokenized credit markets due to the level of control and visibility that blockchain affords. From KYC/AML protocols built into lending smart contracts to advanced risk monitoring dashboards, blockchain technology is creating a data-rich environment that meets the stringent requirements of professional investors.

By integrating real world asset tokenization with on-chain governance and third-party audits, many DeFi lending platforms are positioning themselves as credible alternatives to traditional fixed-income instruments. These developments are catching the attention of blockchain and digital asset consulting firms, who are now advising clients on how to participate safely and strategically in this emerging asset class.

3. Benefits Over Traditional Fixed-Income Instruments

Tokenized private credit is not just a novel technological application—it’s a strategic evolution of fixed-income investing. In contrast to conventional instruments such as corporate bonds or syndicated loans, tokenized credit vehicles offer a modernized framework for yield generation, transparency, and accessibility. As the financial world moves toward a more digital and decentralized future, tokenized private credit stands out by addressing many of the long-standing inefficiencies found in traditional debt markets.

Let’s explore the core advantages in greater detail:

Accessibility: Democratizing Private Credit

Traditional private credit markets have long been the domain of institutional investors—pension funds, hedge funds, and high-net-worth individuals—with high capital requirements and complex onboarding processes. Retail investors and smaller institutional players were often locked out due to regulatory constraints, high fees, and a lack of access to deal flow.

Tokenization removes many of these barriers. Through fractionalized digital tokens, investors can now participate in lending pools or own portions of private loans with significantly lower minimum investment thresholds. A loan that would traditionally require a $500,000 buy-in can now be split into $500 tokenized shares, expanding access to a far broader pool of participants.

This transformation is being championed by digital asset consulting for startups, who see tokenized lending as a path to inclusivity within the private debt landscape.

For example, platforms like Goldfinch and Maple Finance offer tokenized access to credit markets that were once completely off-limits to non-institutional players. These systems also appeal to crypto investment companies seeking diversified sources of yield amid volatile digital asset markets.

Efficiency: Automation and Streamlined Workflows

Traditional fixed-income transactions often involve a cumbersome array of intermediaries, documentation, and manual verification steps. From underwriting to settlement, these layers increase the time required to execute trades and add unnecessary complexity to portfolio management.

Tokenized private credit platforms leverage smart contracts and blockchain automation to streamline these workflows. Loan agreements are coded into smart contracts that automatically enforce terms, manage payment schedules, and handle default triggers—eliminating the need for back-office reconciliation or manual follow-ups.

Moreover, settlements that used to take several days—or even weeks—can now occur in near real-time, improving liquidity and giving investors faster access to their capital. This efficiency aligns with the goals of digital asset investment solutions providers, who aim to maximize operational speed while minimizing risk.

Cost-Effectiveness: Reducing Intermediary-Driven Fees

In the legacy financial system, private credit deals typically incur high costs due to the involvement of multiple third parties—law firms, fund administrators, custodians, brokers, and banks. Each party charges fees, and these costs ultimately reduce net returns for investors and borrowers alike.

With tokenized credit, many of these intermediaries become obsolete. Blockchain’s decentralized architecture allows for direct peer-to-peer lending, drastically reducing overhead. For instance, protocols such as Centrifuge and Credix allow lenders to connect directly with borrowers via on-chain smart contracts that handle everything from KYC/AML compliance to repayment schedules.

For DeFi finance consulting services, this cost efficiency is a powerful value proposition. It allows for the creation of leaner, more transparent financial products that can compete directly with traditional debt instruments on both yield and ease of access.

Real-Time Updates: Enhanced Visibility and Control

One of the persistent frustrations in traditional fixed-income investing is the lack of real-time information. Investors often have to rely on periodic reports, delayed fund statements, or opaque third-party data to understand how their assets are performing.

In contrast, blockchain-based lending platforms provide real-time transparency. All transactions, from loan origination to repayment, are recorded on-chain and can be viewed instantly by authorized parties. Investors can monitor cash flows, assess borrower health, track interest payments, and even participate in governance decisions for lending pools—all from a unified dashboard.

This granular visibility is especially appealing to cryptocurrency investment solutions providers who are focused on accountability and auditability. With on-chain data, reporting is not only faster—it’s more accurate and verifiable.

An example of this transparency is seen with Clearpool, a decentralized credit marketplace where lenders can view borrower profiles, creditworthiness, historical performance, and yield opportunities in real time. This visibility helps both stablecoin investment consultants make informed decisions without waiting for quarterly updates or third-party analyses.

Supplementary Benefits

- Customizable Exposure: Tokenized structures can offer access to specific loan types (e.g., SME loans, emerging market debt, invoice financing), allowing investors to tailor their portfolios based on risk appetite.

- Yield Optimization: As an emerging alternative asset class, tokenized private credit often provides higher yields than government or investment-grade bonds, making it attractive in environments where traditional returns are compressed.

- Integration with DeFi: These instruments can be integrated into broader DeFi fixed incomestrategies—staked, collateralized, or bundled into structured products—providing layered benefits for more sophisticated investors.

4. Key Players in the Ecosystem

The rapid evolution of tokenized private credit has given rise to a dynamic ecosystem of platforms, protocols, and service providers that are redefining how capital is deployed and managed across global markets. These innovators are not just creating new lending infrastructure—they’re building trust, enabling institutional adoption, and proving that decentralized finance can address real-world credit needs.

Below are some of the most influential players helping shape this space:

Goldfinch: Pioneering Undercollateralized Lending in Emerging Markets

Goldfinch is a decentralized credit protocol designed to provide undercollateralized loans to real-world businesses, particularly in underserved regions such as Africa, Latin America, and Southeast Asia. Unlike traditional crypto lending platforms, which typically require borrowers to overcollateralize loans with digital assets, Goldfinch offers credit based on off-chain business fundamentals.

This model is crucial for expanding financial inclusion. For example, a microfinance institution in Kenya can secure a loan from Goldfinch’s lending pools to finance local businesses without holding significant crypto assets. The underwriting process combines blockchain transparency with off-chain data verification, striking a balance between decentralization and real-world practicality.

Goldfinch’s unique community-driven approach also allows individual and institutional lenders—such as crypto investment companies—to provide capital while earning yields. In this way, the platform supports both borrower needs and investor goals within a single, tokenized framework.

Tradable: Bringing Institutional Credit On-Chain

Tradable has emerged as a key player in bridging institutional-grade private credit with blockchain infrastructure. Through strategic partnerships and integrations with protocols such as ZKsync, Tradable has tokenized over $1.7 billion in private credit assets, showcasing the real-world scalability of on-chain debt issuance.

The platform targets larger, more structured credit facilities typically used by banks, credit funds, and asset managers. By creating tokenized representations of these credit instruments, Tradable enables participants to trade or fractionalize exposure via smart contracts, reducing settlement friction and increasing liquidity.

For example, an asset-backed loan to a logistics firm in Europe—previously accessible only via private debt funds—can now be tokenized and sold in portions to a wider range of buyers. Real world DeFi investment consultants are particularly drawn to Tradable’s model, as it introduces efficiencies and transparency to an asset class historically burdened by manual documentation and limited reporting.

Idle Finance: Democratizing On-Chain Private Credit Vaults

Idle Finance is a protocol that curates private credit vaults, giving users access to tokenized loan products backed by real-world borrowers. By leveraging a decentralized infrastructure and integrating with lending platforms such as Credix and Maple, Idle allows users to deploy stablecoins directly into private credit opportunities that yield returns uncorrelated to traditional markets.

One of Idle’s core innovations is its Smart Yield Vaults, which automatically optimize capital allocation across multiple sources of yield, including tokenized credit pools. This makes it particularly appealing for investors seeking consistent income generation with manageable risk exposure.

Idle’s protocol design appeals to digital asset strategy consulting firms, who value automated, secure, and diversified access to fixed-income alternatives. These professionals often incorporate Idle into broader DeFi fixed income portfolios, particularly during periods of rate volatility in traditional bond markets.

Additional Noteworthy Platforms

Beyond these key players, several other platforms are expanding the ecosystem and pushing boundaries:

- Centrifuge: Focuses on connecting real-world assets like invoices, royalties, and trade receivables to DeFi. Their platform enables asset originators to finance real-world debt on-chain using the Tinlake protocol.

- Maple Finance: Offers undercollateralized loans for crypto-native institutions and businesses. Maple’s reputation for managing credit risk through whitelisted pool delegates makes it attractive to digital asset management firmsand cryptocurrency investment consultants seeking vetted opportunities.

- Credix: Based in Latin America, Credix tokenizes private credit for fintech companies and non-bank lenders in emerging markets. Their protocol links global investors to borrowers in regions traditionally underserved by international capital markets.

These platforms represent the intersection of financial innovation, blockchain infrastructure, and global capital allocation. Their success is driving adoption by global digital asset consulting firms who are helping clients navigate this emerging investment frontier.

5. Integration with DeFi Fixed Income Strategies

The convergence of tokenized private credit and DeFi fixed income strategies is revolutionizing the traditional approach to fixed-income investing. By merging real-world lending with decentralized financial infrastructure, a new class of investment opportunities is emerging—one that blends blockchain efficiency with dependable yield mechanisms.

This integration allows both institutional and retail investors to participate in debt-backed digital assets with greater transparency, enhanced liquidity, and increased automation. Below are some of the core strategies and mechanisms that demonstrate how tokenized private credit is being absorbed into the DeFi fixed income landscape.

Yield Farming: Turning Tokenized Credit into a Passive Income Stream

Yield farming, a cornerstone of DeFi, involves deploying digital assets into protocols to earn interest or rewards over time. When applied to tokenized private credit, this strategy becomes even more compelling. Investors can stake credit tokens—such as those representing claims on business loans or trade receivables—into decentralized protocols that automatically distribute yield in the form of additional tokens or fees.

For example, on platforms like Maple Finance or Credix, credit tokens representing undercollateralized loans to fintech companies or small businesses can be locked into yield-bearing smart contracts. In return, investors receive a share of interest repayments, plus governance tokens as incentives for contributing capital. These opportunities are increasingly attractive to stablecoin investment consultants, who see yield farming as a lower-barrier way to generate returns while diversifying exposure beyond volatile crypto assets.

This strategy appeals particularly to fixed-income investors looking for passive income opportunities that maintain relatively low correlation with traditional bond markets.

Liquidity Pools: Deepening Market Access Through Tokenized Lending and Borrowing

Another method for integrating tokenized private credit with DeFi strategies is by pooling assets into decentralized liquidity pools. These pools allow users to lend their credit-backed tokens and earn interest from borrowers, creating an open marketplace for tokenized debt.

Take Idle Finance or Aave Arc, for instance—both platforms offer opportunities for tokenized credit instruments to be added to curated liquidity pools. These pools facilitate decentralized borrowing and lending in a trust-minimized environment, backed by smart contracts that handle all settlements, collateral requirements, and liquidation protocols.

For example, an investor might contribute tokenized SME loans into a pool alongside other participants. Businesses seeking working capital can then borrow from the pool using tokenized assets as collateral. The smart contract ensures repayment terms are enforced, interest rates are adjusted based on supply-demand dynamics, and yields are automatically distributed to liquidity providers.

This model enables blockchain and digital asset consulting firms to help clients navigate risk-managed exposure to DeFi lending markets while staying aligned with relevant regulations and transparency practices.

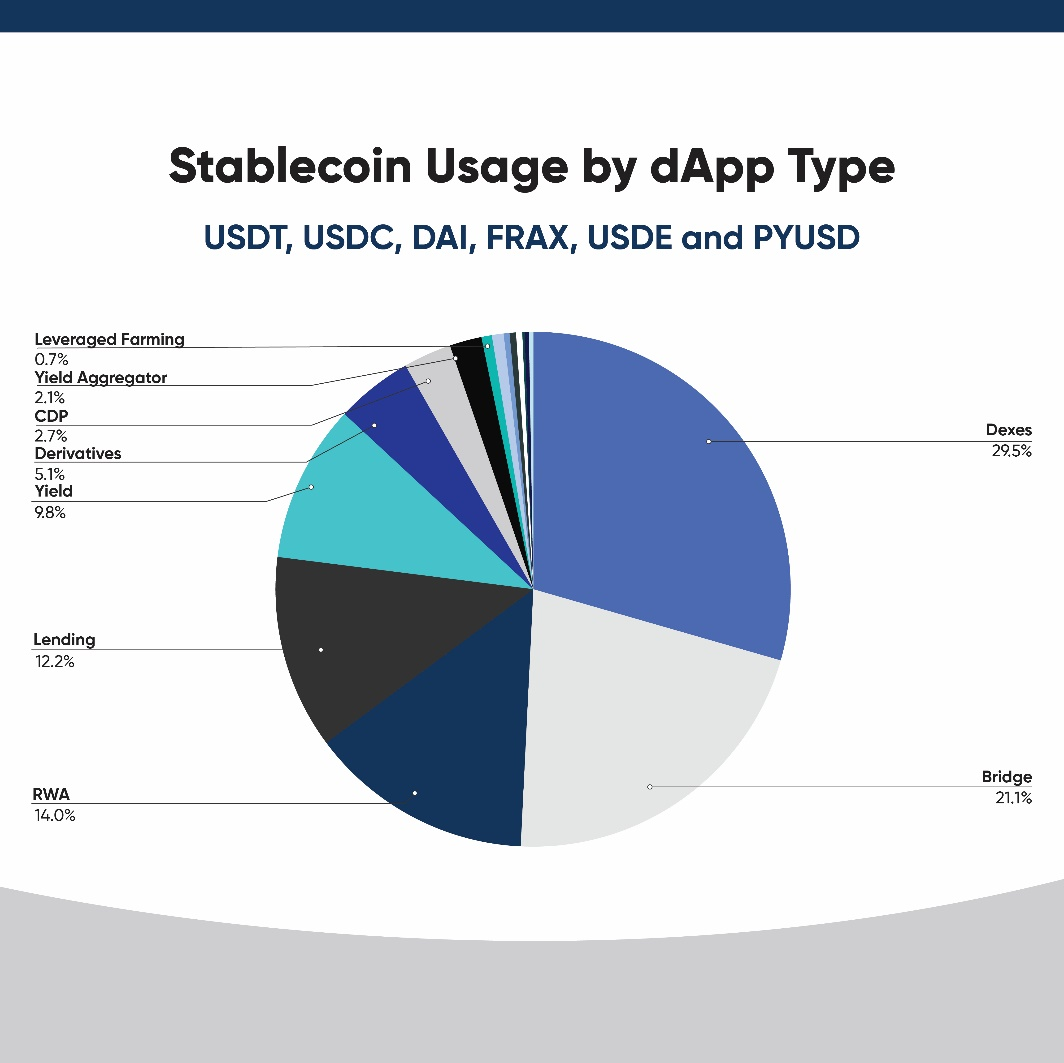

Stablecoin Integration: Reducing Volatility and Enhancing Operational Stability

The use of stablecoins is fundamental to many tokenized private credit strategies within DeFi. These digital currencies—pegged to the value of fiat assets such as the U.S. dollar—enable seamless transactions, payment settlement, and capital deployment across blockchain networks without the price volatility typically associated with cryptocurrencies like Bitcoin or Ethereum.

When used in private credit transactions, stablecoins like USDC, DAI, or USDT serve as the preferred medium of exchange for loan origination, repayment, and yield disbursement. For example, a business in Brazil may borrow $500,000 in USDC via a protocol like Centrifuge, secured against future receivables. Lenders in Europe, Asia, or North America can participate in this opportunity without worrying about currency conversion or volatility risk.

This feature is particularly attractive to cryptocurrency investment consultants who cater to investors with specific risk tolerances and require consistent, fiat-equivalent income streams.

Stablecoins also support the growing practice of real-time interest payments. Instead of waiting for monthly or quarterly repayments as is customary in traditional bonds, investors can receive daily or even hourly yield streams, facilitated entirely through smart contracts—another step toward programmable finance.

Expanding Institutional Interest and Strategic Use Cases

Institutional asset managers and traditional finance players are beginning to explore DeFi fixed income strategies involving tokenized credit, especially in emerging markets and high-yield niches. These use cases often include:

- Trade Finance: Where exporters tokenize invoices and offer them at a discount to liquidity providers, enabling immediate cash flow.

- SME Lending: Where small-to-mid-sized enterprises (SMEs) gain access to working capital, while token holders earn interest with full visibility into loan terms.

- Climate-Focused Lending: Where green bonds and sustainability-linked loans are tokenized and distributed via DeFi platforms, attracting impact investors and ESG-focused funds.

In each case, DeFi real world assets investment consultants play a pivotal role in guiding stakeholders through the technological, regulatory, and strategic dimensions of tokenized lending.

6. Regulatory Landscape and Compliance

As tokenized private credit continues to evolve, its long-term viability hinges on how well it aligns with global regulatory frameworks. The decentralized nature of blockchain technology often challenges traditional compliance models, but navigating this terrain is essential for fostering institutional confidence, minimizing legal risks, and ensuring sustainable market growth. From robust identity verification protocols to region-specific licensing requirements, understanding the complexities of regulation is a foundational step for all stakeholders involved—especially those providing digital asset consulting for compliance.

Compliance Requirements: Upholding KYC and AML Standards

Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols are two of the most critical regulatory pillars in digital asset markets. In the context of tokenized private credit, these requirements help ensure that the originators of loans, the platforms facilitating tokenization, and the investors purchasing the assets are all operating transparently and legally.

For instance, platforms like Maple Finance and TrueFi have embedded KYC/AML procedures directly into their onboarding processes. Institutional users must verify their identities, provide financial disclosures, and adhere to jurisdictional compliance checks before participating in lending pools. This level of diligence is necessary to prevent fraudulent actors from exploiting decentralized systems for illicit activities such as money laundering or terrorism financing.

Digital asset strategy consulting firms often play a crucial role in helping startups and established firms design compliance-ready tokenization protocols that meet global regulatory standards, while also maintaining user privacy through cryptographic identity solutions and zero-knowledge proofs.

Jurisdictional Variances: Adapting to a Fragmented Global Framework

One of the most challenging aspects of regulating tokenized private credit lies in its cross-border nature. Laws governing securities, lending, and blockchain-based assets vary significantly from one jurisdiction to another. For example:

- In the U.S., the Securities and Exchange Commission (SEC) often classifies tokenized credit instruments as securities, triggering rigorous disclosure and registration requirements under existing securities laws.

- In Switzerland, a more blockchain-friendly regulatory framework categorizes certain digital assets as DLT securities, facilitating easier issuance and trading.

- In Singapore, the Monetary Authority of Singapore (MAS) has created a regulatory sandbox to encourage innovation while ensuring that companies comply with AML, CFT (Combating the Financing of Terrorism), and financial conduct regulations.

For this reason, global digital asset consulting firms and real world asset consultants are often called upon to help organizations craft jurisdiction-specific strategies. These may involve incorporating in favorable regions, working with legal partners in each country of operation, or employing compliance-focused blockchain protocols that adapt to legal updates in real time.

The ability to demonstrate regulatory alignment is particularly important for institutional investors, many of whom are bound by fiduciary duty to engage only with compliant, low-risk products.

Security Considerations: Protecting Smart Contracts and User Funds

Regulatory compliance is not only about paperwork and jurisdictional approval—it also involves technical safeguards that ensure the integrity and safety of tokenized systems. Smart contracts, which power the automation behind tokenized private credit platforms, must be thoroughly audited and stress-tested to avoid vulnerabilities that could lead to financial losses or data breaches.

Security failures have already been costly in DeFi. In 2022, the Beanstalk Protocol suffered a $182 million exploit due to a governance loophole. Similarly, flash loan attacks on Cream Finance and bZx highlighted the need for stricter contract security and operational due diligence.

This has led to the rise of specialized digital assets consulting services focused on cybersecurity, penetration testing, and third-party auditing. These services help crypto asset management firms and digital asset management companies ensure their credit tokenization frameworks are secure before going live. Moreover, platforms now frequently offer bug bounty programs—financial rewards for developers who discover and report flaws—helping strengthen community trust and regulatory defensibility.

Ensuring operational and code-level security is not just a best practice—it’s increasingly becoming a prerequisite for licensing and compliance approval in key markets.

7. Challenges and Considerations

Despite the growing momentum behind tokenized private credit, the sector is not without its hurdles. While the benefits are clear—greater accessibility, enhanced liquidity, and more efficient credit allocation—the industry must still contend with a number of structural, technical, and regulatory challenges. Addressing these issues will be essential for the long-term success and institutional adoption of tokenized debt products, especially for players offering blockchain asset consulting.

Technological Barriers: Interoperability and Scalability Remain Complex

One of the core technical challenges facing the sector is interoperability—the ability for different blockchain platforms, protocols, and financial systems to communicate and share data seamlessly. In the current landscape, many tokenized credit products are built on different blockchains (Ethereum, Solana, Avalanche, etc.), each with its own token standards, consensus mechanisms, and compliance toolkits.

This fragmentation complicates both user experience and institutional integration. For example, an investment analysis and portfolio management platform that supports tokenized credit on Ethereum may not be able to track or interact with assets tokenized on Polygon without additional middleware or bridging infrastructure. Projects like Chainlink’s Cross-Chain Interoperability Protocol (CCIP) and LayerZero are working to solve this issue, but widespread, secure adoption is still a work in progress.

Scalability is another pressing concern. As more users and transactions enter the system, network congestion and high gas fees (particularly on Ethereum) can reduce efficiency. While Layer 2 solutions like Arbitrum and Optimism offer promising improvements, ensuring these solutions are secure and compatible with credit tokenization processes will require further innovation.

Market Adoption: Educating Investors and Earning Trust

Despite the advancements in blockchain asset investments consulting, one of the biggest obstacles remains investor education and psychological adoption. Traditional fixed-income investors—especially those managing pensions, endowments, or insurance funds—tend to favor predictability, transparency, and regulatory certainty. The idea of earning yield from decentralized, tokenized loans still appears risky or overly complex to many of them.

Moreover, high-profile failures in the crypto industry, such as the collapse of TerraUSD, Celsius, and FTX, have shaken public confidence in digital assets. While these were not directly tied to tokenized private credit, the negative perception of the broader crypto space can discourage institutional and retail interest alike.

This is where digital asset strategy consulting firms can play a transformative role. By offering educational campaigns, compliance walkthroughs, and onboarding support, these firms can help demystify tokenized credit products and encourage safe, strategic participation in the market.

A real-world example is Goldfinch, which has made concerted efforts to explain the mechanics and risks of undercollateralized lending to its community through whitepapers, blog posts, and governance forums. Similarly, platforms like Maple Finance regularly publish credit assessments and performance reports to build trust and attract institutional clients.

Regulatory Uncertainty: Navigating an Evolving Legal Landscape

Regulatory ambiguity remains one of the most significant barriers to scaling tokenized private credit. In many jurisdictions, there is still no clear legal definition for tokenized debt instruments. Are they securities? Are they commodities? Do they fall under lending regulation or digital asset frameworks? The answers vary dramatically by country—and often even within regions of the same country.

For instance:

- In the United States, the Securities and Exchange Commission (SEC) has taken an aggressive stance, often classifying tokenized assets as unregistered securities, creating uncertainty for DeFi platforms.

- In Germany, regulators have introduced a framework that allows blockchain-based securities under the Electronic Securities Act, signaling a more forward-thinking approach.

- In Hong Kong and Switzerland, regulatory sandboxes are enabling real-world testing of tokenized lending products with regulatory oversight.

This fragmented landscape makes it difficult for platforms to scale globally without extensive legal coordination. It also discourages risk-averse investors who prefer to avoid assets subject to ambiguous or shifting regulation.

This is where compliance-focused digital asset consulting firms offer value. These specialists provide tailored regulatory guidance, help obtain licenses, and design legally sound smart contracts—reducing risk for both issuers and investors.

Additionally, tokenization platforms must be equipped to handle jurisdiction-specific compliance checks, including KYC/AML, tax reporting obligations, and investor accreditation. Ignoring these issues could result in regulatory penalties, user losses, or forced shutdowns.

8. Future Outlook

The future of tokenized private credit appears increasingly promising as technology, regulation, and market demand begin to align in ways that support meaningful growth and sustainable adoption. As a convergence point between traditional finance and decentralized infrastructure, tokenized private credit is not just a passing innovation—it is poised to become a cornerstone of modern fixed-income strategy, particularly for institutional investors and sophisticated asset managers seeking alternative sources of yield in a shifting global landscape.

Institutional Adoption: A New Era of Credit Participation

Institutional interest in digital assets has steadily grown, and tokenized private credit is emerging as a compelling use case for those seeking yield-generating exposure without the volatility of public cryptocurrencies. As platforms evolve and regulatory clarity improves, institutions such as pension funds, asset managers, insurance companies, and private equity firms are increasingly considering blockchain-enabled lending as part of their diversified investment strategies.

A key driver of this adoption is the ability to customize and control credit exposures with unparalleled transparency. Smart contracts can embed detailed risk parameters, enable real-time auditing, and automate performance reporting—capabilities that traditional private credit markets often lack. For instance, Maple Finance has already attracted participation from institutional lenders by offering clear underwriting standards and verified borrower profiles on-chain.

Additionally, the availability of digital asset consulting for compliance ensures that institutional participants can navigate regulatory requirements, conduct due diligence, and structure investments in line with governance standards. This layer of support makes digital asset management services more viable for firms operating under strict fiduciary obligations.

Innovation: Advancements in Technology and Protocol Design

The rapid pace of innovation in blockchain technology is expected to further accelerate the capabilities of tokenized lending platforms. One of the most significant areas of development is on-chain credit scoring. Emerging protocols are experimenting with integrating off-chain financial data (via oracles or decentralized identity systems) to better assess borrower risk. Platforms such as Centrifuge and Goldfinch have already begun incorporating real-world credit data into their lending models, allowing for more accurate pricing and risk allocation.

Other innovations include:

- Composable finance structures, where tokenized credit instruments can interact with other DeFi primitives like options, insurance, or yield strategies.

- AI-powered risk analytics, enhancing loan approval and default prediction models within the tokenized ecosystem.

These advancements will lead to a more efficient, secure, and user-friendly experience, enabling crypto investment companies to craft bespoke fixed-income products tailored to evolving market needs.

Global Expansion: Unlocking Capital in Emerging Economies

One of the most exciting frontiers for tokenized private credit is its potential impact on emerging markets. Many regions in Latin America, Africa, Southeast Asia, and Eastern Europe face persistent challenges accessing affordable, transparent capital. Traditional banking systems often exclude small businesses and entrepreneurs due to high credit risks, limited collateral, or bureaucratic inefficiencies.

Tokenization can disrupt this dynamic by enabling peer-to-peer credit channels that operate outside of conventional gatekeepers. For example, a small manufacturing business in Kenya could access working capital through a decentralized credit pool on Celo or Polygon, backed by tokenized real-world receivables and governed by transparent smart contracts. Platforms like Goldfinch are already pioneering this model, offering undercollateralized loans to businesses in Nigeria, the Philippines, and India—facilitated through decentralized governance mechanisms.

In these regions, RWA DeFi investment consultants can play a critical role in structuring compliant, culturally contextualized financial products that foster sustainable development.

Furthermore, stablecoins for investment—such as USDC or GHO—offer a reliable medium of exchange in countries with volatile local currencies. Their integration into tokenized lending markets allows borrowers to access capital in a stable currency while giving investors a hedge against inflation or devaluation risk.

Final Thoughts

Tokenized private credit is not simply an evolution of private debt markets—it represents a paradigm shift. By embedding credit within programmable digital assets, investors and borrowers alike gain access to a financial architecture that is more transparent, efficient, and globally accessible. With continued innovation and responsible development, tokenized credit products could very well redefine the future of fixed income, particularly as part of broader digital asset portfolio management frameworks and crypto asset management solutions.

This new frontier will be shaped by the collaborative efforts of blockchain developers, institutional investors, global digital asset consulting firms, and forward-thinking regulators—all working to unlock capital, reduce barriers, and drive innovation in the debt markets of tomorrow.

Start Navigating the Future of Digital Asset Strategies with Confidence

Discover how Kenson Investments’ educational resources and market insights can help you explore blockchain-based opportunities and emerging investment structures.

Work with Kenson Investments’ digital asset specialists to begin your journey toward informed, future-focused decision-making.