Stablecoins—digital assets pegged to fiat currencies—have evolved from niche financial instruments to pivotal tools in global economic strategy. As central banks develop Central Bank Digital Currencies (CBDCs) and private entities issue their own stablecoins, a complex geopolitical landscape emerges. This blog delves into how nations and financial institutions leverage stablecoins to gain economic influence, examining the competition between private stablecoins, CBDCs, and decentralized alternatives, and their impact on global trade, inflation hedging, and capital controls.

The Rise of Stablecoins in Global Finance

Stablecoins have seen exponential growth, with the market capitalization reaching $235 billion, up from $152 billion a year prior. Their appeal lies in price stability, making them attractive for traders and individuals in high-inflation countries. Major players like Tether (USDT) and Circle (USDC) dominate the market, providing alternatives to traditional banking systems.

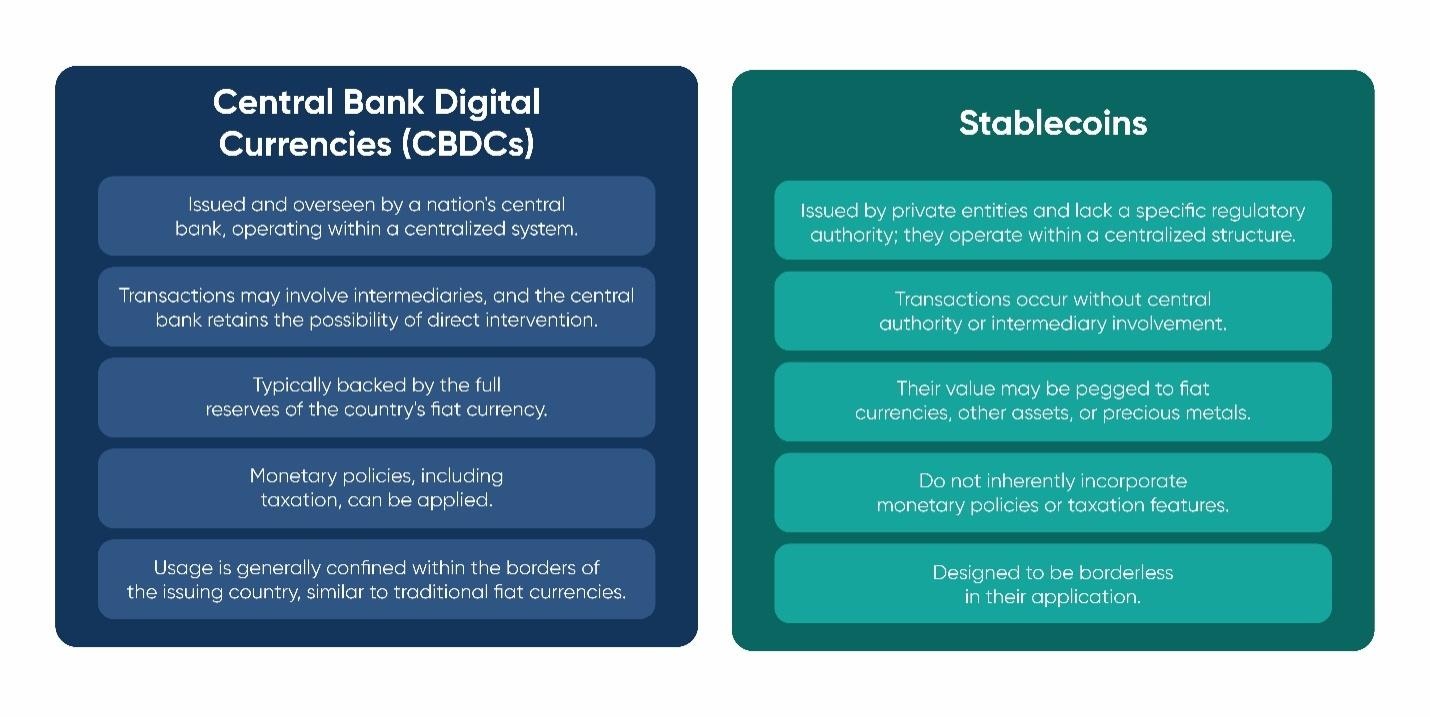

CBDCs vs. Private Stablecoins: A Strategic Tug-of-War

Central banks worldwide are exploring CBDCs to modernize payment systems and maintain monetary sovereignty. Over 70% are considering CBDC issuance, aiming to improve financial inclusion and payment efficiency. However, private stablecoins offer advantages in cross-border transactions and innovation. Tether’s CTO, Paolo Ardoino, argues that CBDCs will not impact private stablecoins significantly, as they serve different purposes and infrastructures.

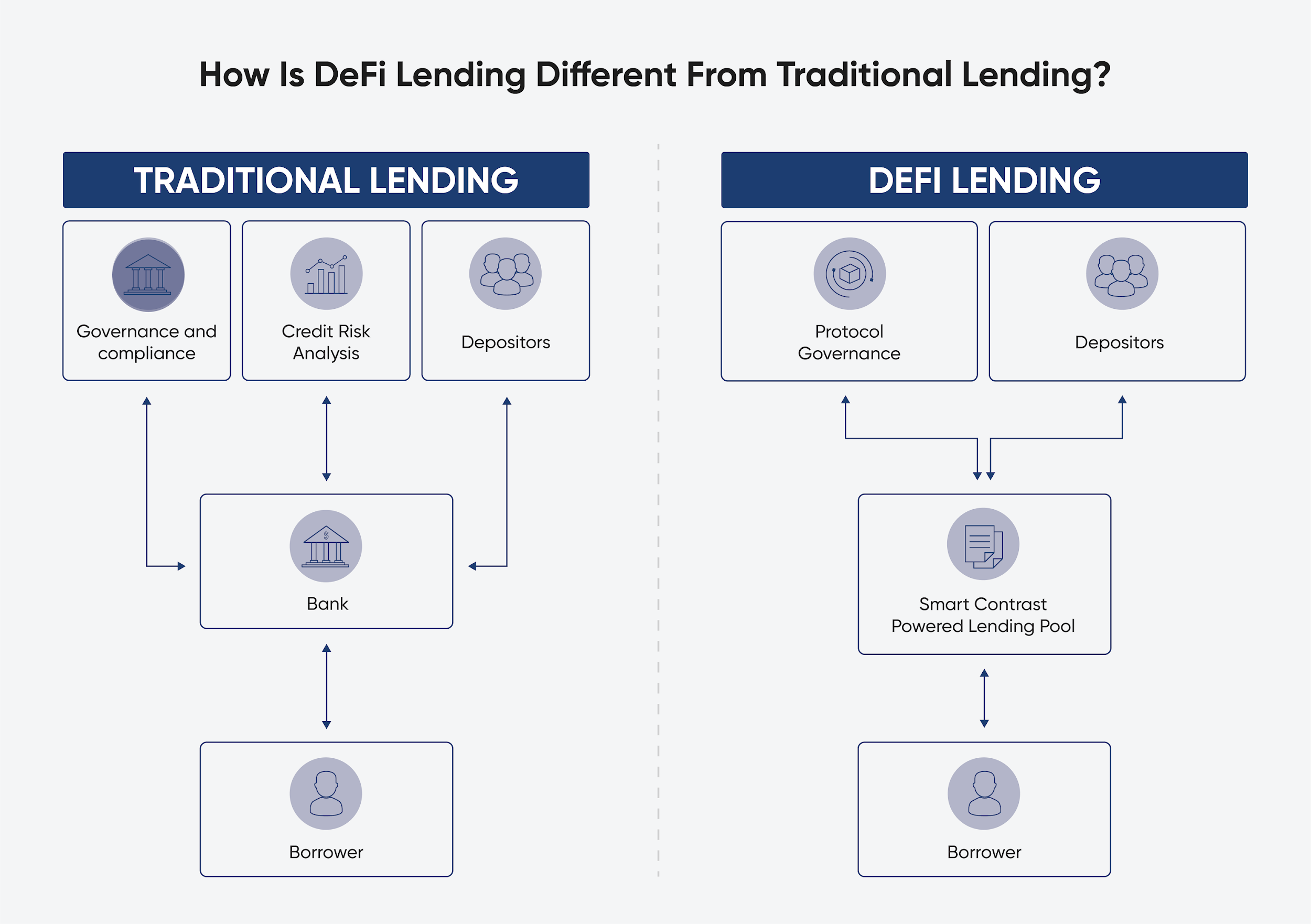

Decentralized Stablecoins – A Forgotten Front in the Geopolitical Race?

Decentralized stablecoins, such as MakerDAO’s DAI and Frax’s partially algorithmic model, offer a censorship-resistant alternative to centralized stablecoins. Though smaller in market cap, their ability to operate autonomously across DeFi platforms adds a layer of resilience against regulatory overreach.

Yet, their growth has been stunted due to volatility in collateral assets and lack of regulatory frameworks. Nevertheless, DeFi finance consulting services are helping startups build new decentralized models that can maintain peg stability while aligning with emerging global norms.

CBDC Infrastructure – Global Developments and Use Cases

The Bahamas pioneered the first fully deployed CBDC, the Sand Dollar, now accepted at dozens of local merchants and integrated with mobile banking. China’s e-CNY has reached over 260 million users in pilot cities and is used for public transportation, government disbursements, and salary payments. India’s digital rupee pilot, launched in December 2023, targets wholesale and retail settlement efficiency.

However, critics argue that these CBDCs may enable greater state surveillance and programmable monetary policies. Unlike decentralized stablecoins, CBDCs are state-controlled, creating a fundamental divergence in vision that shapes stablecoin geopolitics.

Regulatory Clarity and Political Support

The regulatory environment for stablecoins is no longer in a state of ambiguity—it’s actively maturing. In 2024, the U.S. Congress placed digital asset legislation high on its agenda, reflecting growing recognition of stablecoins as core infrastructure for modern financial systems. Several pivotal bills are shaping this landscape with bipartisan backing, offering long-awaited clarity to both individual and institutional market participants.

Two major proposals—the Stablecoin Transparency Act (STABLE Act) and the Guarding Against Illicit Finance Using Stablecoins (GENIUS Act)—aim to establish comprehensive oversight. These bills propose requirements for full reserve backing, regular audits, and the issuance of stablecoins only through licensed entities. For institutional players, such mandates represent not only enhanced investor protection but also an opportunity to operate within a more secure and trusted environment.

Complementing these efforts is the Financial Innovation and Technology for the 21st Century Act (FIT21), which proposes a clear framework to define the jurisdictional boundaries between the Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC). FIT21 aims to treat payment-focused stablecoins as non-securities, a classification that could unlock broader usage by payment processors, fintechs, and traditional financial institutions alike.

This regulatory momentum is being driven by a strategic understanding of stablecoins’ potential to modernize payments, streamline trade, and support financial inclusion. According to a 2024 survey by Coinbase and Morning Consult, 63% of U.S. voters believe the country should lead in digital asset innovation, and more than half support regulatory clarity that would protect consumers without stifling innovation.

These public sentiments are being echoed in Washington. High-profile figures like Senator Kirsten Gillibrand and Representative Patrick McHenry have voiced strong support for stablecoin legislation that balances innovation with risk mitigation. In a June 2024 Senate hearing, McHenry emphasized that “regulatory certainty is the missing link between crypto’s potential and its full-scale integration into our financial system.”

This clarity is not only reassuring for consumers—it’s catalyzing institutional adoption. As crypto investment firms and digital asset strategy consulting firms work with clients to incorporate stablecoins into broader portfolios, having a well-defined compliance framework allows them to do so safely and at scale.

On a global level, the United Kingdom, Singapore, and the European Union are taking similar steps. The EU’s Markets in Crypto-Assets (MiCA) regulation—set to be fully enforced by 2025—requires stablecoin issuers to maintain adequate reserves, undergo licensing, and adhere to operational transparency. These regulations not only legitimize stablecoins within traditional finance but also invite participation from digital asset management companies and global financial institutions seeking compliant exposure.

Political Lobbying and Stablecoin Influence in Washington

Stablecoin regulation has become one of the most hotly debated issues in Washington, and crypto firms are stepping up their political involvement to shape the narrative. According to a 2024 report from The Economist Intelligence Unit, digital asset corporations—including stablecoin issuers like Circle and Coinbase—have emerged as the largest corporate political donors in the United States, outpacing traditional banking institutions. Collectively, Coinbase, Kraken, and Circle funneled over $54 million into lobbying efforts during the 2023–2024 election cycle, reflecting the sector’s intent to influence stablecoin legislation and digital asset policy.

Industry organizations such as the Blockchain Association and the Chamber of Digital Commerce have been instrumental in pushing for a clear, uniform federal regulatory framework for stablecoins. Their advocacy focuses on classifying stablecoins as payment tools rather than securities, a distinction that directly impacts how these instruments are taxed, audited, and adopted by mainstream financial institutions.

This push has gained significant traction. Bipartisan bills introduced in both the House and Senate—including the Clarity for Payment Stablecoins Act and the Digital Dollar Pilot Program—indicate growing consensus in favor of tailored legislation for privately issued stablecoins. U.S. Representative Patrick McHenry, Chair of the House Financial Services Committee, recently noted that “clear stablecoin rules are essential for maintaining American competitiveness in the digital currency landscape.”

Prominent institutional voices echo this sentiment. Larry Fink, CEO of BlackRock, stated during a 2024 Bloomberg interview that “Stablecoins could be a transformative force in global payments—regulation should enable innovation, not stifle it.” This kind of public endorsement from traditional financial powerhouses reinforces confidence in stablecoin infrastructure as a credible asset class.

For digital asset management companies, these political developments signal a maturing policy environment that supports institutional-grade compliance, risk management, and long-term investment viability. Regulatory clarity doesn’t just benefit crypto-native firms—it empowers banks, hedge funds, and fintech platforms to confidently integrate stablecoins into payment rails, custody services, and digital asset investment solutions.

Geopolitical Implications and Economic Influence

Stablecoins are becoming tools for economic influence. Countries like China are advancing their CBDC projects, while private stablecoins challenge traditional financial systems. The competition between CBDCs and private stablecoins reflects broader geopolitical dynamics, with nations aiming to assert control over digital financial ecosystems.Cointelegraph

The Role of Stablecoins in Sanction Evasion and Capital Flight

While stablecoins provide clear utility in financial inclusion and cross-border trade, they are also being scrutinized for enabling capital flight and sanctions evasion. For instance, U.S. Treasury reports have flagged stablecoin usage in North Korea’s cybercrime operations and capital movement in regions like Venezuela and Lebanon. In 2023, Elliptic traced over $7 billion in illicit funds moved through USDT, highlighting regulatory blind spots.

These concerns are central to why regulatory clarity—especially around digital asset consulting for compliance—is critical. Striking the balance between innovation and control is driving legislative urgency across the U.S., EU, and Asian markets.

Stablecoins and Global Trade Settlement

As geopolitical uncertainty, de-dollarization trends, and cross-border payment inefficiencies mount, stablecoins are emerging as viable alternatives to traditional correspondent banking systems. Backed by fiat or real-world assets, these digital instruments are increasingly being leveraged for faster, cheaper, and politically neutral trade settlements—especially in regions grappling with currency volatility, capital controls, or financial exclusion.

According to the Bank for International Settlements (BIS) 2023 Innovation Hub report, over 60% of surveyed central banks and financial institutions are actively exploring digital assets—primarily stablecoins—for real-time cross-border payments. The appeal lies in stablecoins’ ability to reduce transaction costs, cut settlement times from days to seconds, and operate 24/7 outside of legacy systems like SWIFT.

This institutional curiosity is translating into real-world deployments. Circle’s USDC has been integrated into fintech platforms across Southeast Asia, such as Coins.ph in the Philippines and GrabPay in Singapore, offering digital asset investment solutions that cater to remittances and regional trade payments. In Latin America, Argentina and Brazil have seen rising usage of stablecoins like USDC and USDT in B2B trade, especially among small-to-medium enterprises that face currency instability and limited access to U.S. dollars.

The strategic value of stablecoins is not lost on policymakers either. In early 2024, Russia’s Ministry of Finance and Iran’s Central Bank confirmed joint discussions around a gold-backed stablecoin aimed at bypassing U.S. sanctions and facilitating regional commerce. While still in early stages, this proposal underscores how stablecoin geopolitics are increasingly tied to sovereign efforts to reclaim monetary autonomy and hedge against inflationary risk—especially as the U.S. dollar’s dominance in global trade faces mounting pressure.

Further, as stablecoins evolve beyond retail use into institutional-grade tools, we’re witnessing the emergence of blockchain asset investments consultants that guide sovereign funds, multinational banks, and fintechs in leveraging these instruments for trade finance, treasury operations, and international settlements.

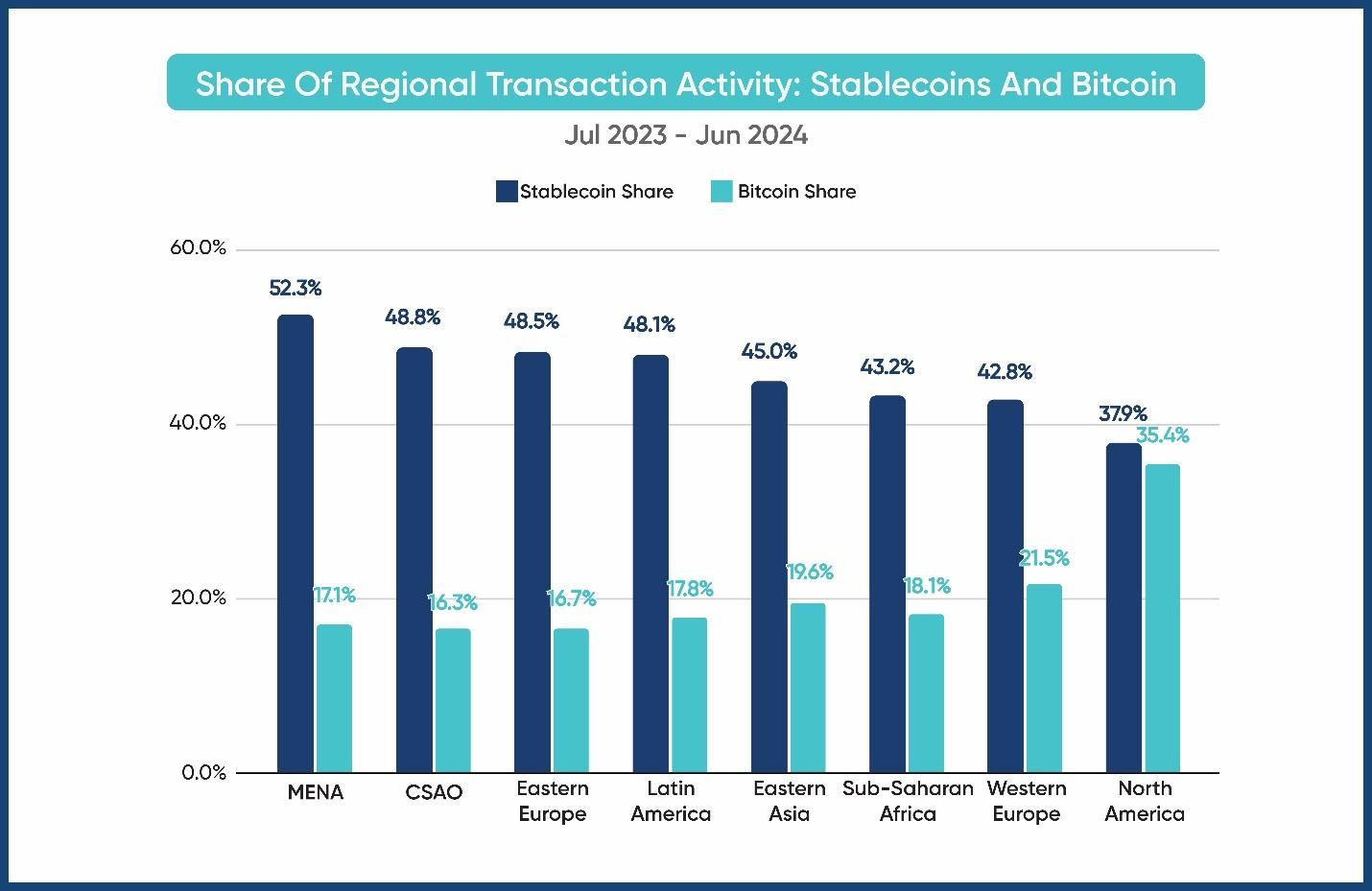

A 2024 study by Chainalysis found that stablecoin usage in cross-border transactions grew 40% year-over-year, with significant traction in Africa, Southeast Asia, and the Middle East—regions traditionally underserved by global banking infrastructure. These developments are not just technical upgrades; they are reshaping global economic alignment, enabling trade partnerships that are less dependent on Western financial intermediaries.

Political support is quietly building in advanced economies as well. The European Commission’s Markets in Crypto-Assets (MiCA) framework, effective in 2024, allows authorized stablecoins to operate within the EU under clear supervision—potentially enabling euro-backed stablecoins to support intra-European trade. In the U.S., legislative proposals such as the Clarity for Payment Stablecoins Act signal growing bipartisan interest in treating stablecoins as regulated payment instruments rather than securities, aligning with how major payment processors are beginning to use them in corporate settlements.

The growing consensus among economists and fintech leaders is that stablecoins—when paired with proper oversight—can dramatically increase the efficiency, transparency, and accessibility of global trade finance. As crypto asset management frameworks mature and regulation brings clarity, stablecoins for investment and settlement are gaining institutional legitimacy, not just speculative appeal.

For companies navigating these shifts, working with a digital asset management company can provide the expertise needed to incorporate stablecoins into strategic trade operations. From compliance consulting to portfolio management of stablecoin reserves, these services are quickly becoming essential for international market participants.

How Developing Economies Are Leveraging Stablecoins

In countries plagued by hyperinflation or capital controls, stablecoins are being used as inflation hedges and a means of preserving purchasing power. In Nigeria, for instance, over 33% of crypto transactions involve stablecoins, primarily USDT, according to Chainalysis 2024 data. Argentina’s black market for U.S. dollars has led to widespread adoption of USDC and USDT among citizens and small businesses as a workaround to currency restrictions.

These developments point to a shift where stablecoins are not only speculative instruments but practical financial tools for everyday survival, remittance, and commerce. In this context, private stablecoins often outperform CBDCs in adoption and use due to greater accessibility and privacy.

Institutional Investments and Market Confidence

The stablecoin ecosystem is rapidly maturing, thanks in large part to rising institutional involvement—an essential signal of growing legitimacy and trust in digital assets. In 2024, over $120 billion in institutional capital was allocated to blockchain-based financial instruments globally, according to data from PwC’s Global Crypto Hedge Fund Report. A significant portion of this capital is flowing into regulated stablecoin frameworks, with financial giants such as Bank of America, JPMorgan Chase, and PayPal exploring deployment strategies tied to programmable money and blockchain settlement.

For instance, PayPal’s launch of PYUSD, a dollar-backed stablecoin issued in partnership with Paxos, marked one of the first instances of a publicly traded U.S. company offering a compliant, consumer-facing stablecoin product. Simultaneously, Bank of America has acknowledged in a recent research note that stablecoins “represent the future of frictionless payments”—with the potential to streamline remittances, reduce costs in cross-border settlements, and enhance treasury operations for institutional clients.

These developments are not occurring in isolation. The Bank for International Settlements (BIS) noted in a 2024 report that 76% of central banks are actively engaging with private-sector partners to explore interoperability between central bank digital currencies (CBDCs) and private stablecoins. This growing alignment between public and private institutions indicates confidence not just in the concept of stablecoins, but in their long-term role within global finance.

Importantly, this influx of institutional interest is coupled with regulatory tailwinds. The proposed U.S. Payment Stablecoin Act would establish a licensing regime under the Federal Reserve, allowing federally regulated entities—such as banks, credit unions, and digital asset management companies—to issue or manage stablecoins under strict guidelines. The clarity offered by such frameworks is removing key barriers to entry for financial institutions previously hesitant due to legal ambiguity.

Public sentiment is evolving alongside these institutional moves. A 2024 survey by Fidelity Digital Assets found that 74% of institutional investors now view stablecoins as a viable tool for managing portfolio liquidity and hedging against fiat currency volatility—a sharp rise from just 47% in 2021. This surge reflects growing confidence not only in the underlying technology, but also in the emerging safeguards shaping the ecosystem.

For digital asset strategy consulting firms and blockchain asset investments consultants, this trend underscores the importance of supporting institutions in integrating stablecoins into diversified investment strategies. Stablecoins are no longer speculative instruments; they are becoming foundational tools in treasury operations, payment infrastructure, and regulated wealth preservation strategies.

How Stablecoins Are Being Integrated into Traditional Banking

Stablecoins are no longer viewed solely as crypto-native instruments—they’re rapidly becoming a bridge between traditional banking and blockchain-based finance. Leading global financial institutions are actively integrating stablecoin technologies into their core operations, signaling a shift in how monetary value is stored, transferred, and settled.

JP Morgan Chase has taken a notable lead with its JPM Coin, a blockchain-based stablecoin used for real-time cross-border payments among institutional clients. As of late 2023, JPM Coin had already processed over $1 billion in daily transactions, according to the bank’s own reports. This internal pilot, running on JP Morgan’s Onyx blockchain platform, demonstrates how stablecoins can significantly enhance liquidity management and streamline treasury operations within regulated financial environments.

Meanwhile, fintech innovators are reinforcing this trend. PayPal’s launch of PYUSD in collaboration with Paxos introduced a fully-backed, U.S. dollar-denominated stablecoin available to millions of U.S. users through the PayPal ecosystem. Unlike early stablecoins with opaque backing, PYUSD is audited monthly, ensuring transparency and regulatory alignment—a critical factor in securing consumer trust and encouraging institutional buy-in.

Visa and Mastercard have also embraced stablecoins, piloting USDC (USD Coin) settlements directly on their payment rails. Visa’s 2024 pilot with Crypto.com successfully processed cross-border transactions using USDC over the Ethereum blockchain, while Mastercard has partnered with Consensys and Circle to explore secure blockchain-based settlements. These pilots not only validate the reliability of stablecoins for investment and payments but also suggest that digital asset investment solutions are on track to become a permanent fixture in global finance.

The regulatory climate is catching up to this momentum. The U.S. Office of the Comptroller of the Currency (OCC) has affirmed that federally chartered banks may use stablecoins for payment settlement, provided they follow applicable risk management protocols. This ruling, paired with growing bipartisan political support, is removing previous uncertainty that held traditional banks back from engaging with digital assets.

Industry experts are increasingly vocal about the long-term role of stablecoins in banking. In a 2024 panel hosted by the World Economic Forum, Larry Fink (BlackRock CEO) stated, “Tokenized money and regulated stablecoins are the future of digital banking—they offer precision, speed, and compliance in a way fiat rails cannot.” This sentiment echoes findings from a PwC digital assets survey, which found that 61% of traditional financial institutions plan to integrate stablecoin infrastructure by 2026, either for settlement, cash management, or remittances.

For those seeking tailored support, digital asset management consultants are playing a pivotal role in helping banks and fintechs navigate integration. From compliance and risk assessment to digital asset portfolio management, these firms provide the infrastructure and strategy necessary to support stablecoin adoption at scale.

The takeaway is clear: stablecoins are no longer a fringe concept. They’re now a critical component of evolving global finance—embedded in banking infrastructure, supported by institutional capital, and shaped by improving regulation. As adoption accelerates, informed market participants will find new opportunities in both regulated stablecoin ecosystems and the broader DeFi finance consulting services sector supporting them.

Strategic Considerations for Investors

Investors should consider engaging with a digital asset strategy consulting firm to navigate the evolving landscape. Services such as blockchain asset consulting can assist in aligning investment approaches with current regulations. Additionally, exploring cryptocurrency investment solutions can diversify portfolios and hedge against inflation.

Partner with Kenson Investments

Kenson Investments offers guidance in the digital asset space, providing educational services such as digital asset management consulting and stablecoin investment consulting. Our team of seasoned digital asset specialists assists clients, ensuring alignment with evolving regulations and market trends. Engage with Kenson Investments to navigate the complexities of the digital asset ecosystem confidently.

Disclaimer: The information provided on this page is for educational and informational purposes only and should not be construed as financial advice. Crypto currency assets involve inherent risks, and past performance is not indicative of future results. Always conduct thorough research and consult with a qualified financial advisor before making investment decisions.

“The crypto currency and digital asset space is an emerging asset class that has not yet been regulated by the SEC and US Federal Government. None of the information provided by Kenson LLC should be considered as financial investment advice. Please consult your Registered Financial Advisor for guidance. Kenson LLC does not offer any products regulated by the SEC including, equities, registered securities, ETFs, stocks, bonds, or equivalents”