Part I: When Time Itself Becomes Risk

Executive Overview

For decades, institutional finance relied on time as a stabilizer. Settlement cycles created buffers. Netting windows absorbed volatility. Margin calls arrived in predictable rhythms. End-of-day reconciliation provided space for error correction and funding optimization. That structure is dissolving.

Atomic clearing models, tokenized collateral, programmable cash, and 24/7 blockchain rails are collapsing settlement cycles from days into minutes. In this environment, exposure does not drift gradually toward resolution. It materializes almost immediately. The system no longer tolerates delay.

For allocators evaluating digital asset exposure, this shift is not technological trivia. It directly affects liquidity durability, credit stability, and operational survivability. The move toward real-time financial settlement creates a new form of structural vulnerability: compressed settlement risk, where the disappearance of time eliminates traditional shock absorbers. This paper examines how settlement compression alters risk timing, why traditional assumptions no longer hold, and how disciplined managers must recalibrate frameworks accordingly.

1. The Old Clock: How Settlement Used to Work

Traditional financial markets operated on structured delay. Equity markets settled on T+2 cycles. Derivatives exposures were netted through clearinghouses before final margin obligations were crystallized. Treasury teams optimized funding within daily cycles. Even in volatile periods, there was temporal elasticity built into the system. That elasticity served three quiet but critical purposes.

First, liquidity smoothing. Institutions could allocate funding across a trading day, relying on overnight windows to rebalance exposures. Second, credit netting. Bilateral trades were aggregated, and gross exposures were reduced before settlement. The clearinghouse functioned as a buffer between volatility and funding stress. Third, operational tolerance. Breaks, mismatches, or compliance flags could be resolved before obligations finalized. Settlement was not an event. It was a process unfolding within predictable time corridors.

Even after post-2008 reforms strengthened central clearing and collateral requirements, the underlying assumption remained intact. Risk unfolded over hours and days. Liquidity teams could plan accordingly. The clock was structured.

2. What Compression Changes

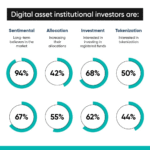

The acceleration of settlement is being driven by tokenization, programmable stablecoins, and blockchain-based clearing rails. By 2025, tokenized U.S. Treasuries exceeded $1.6 billion in circulation on-chain. Real-world asset protocols surpassed $8 billion in locked value. Large institutions have piloted tokenized repo transactions that settle in minutes rather than overnight.

These systems are not simply faster versions of traditional rails. They remove the separation between execution and settlement. In atomic environments, ownership transfer and payment occur simultaneously. A trade either completes instantly or fails instantly. There is no deferred window.

This is the essence of compressed settlement risk. When settlement finality collapses into trade execution, liquidity exposure and operational risk converge at the same moment. Duration risk decreases. Liquidity sensitivity increases. That trade-off is not neutral.

3. The Disappearance of Grace Periods

Under traditional cycles, volatility had a rhythm. A sharp price move at mid-morning could still be absorbed within daily funding windows. Margin calls were recalculated at scheduled intervals. Treasury desks had structured time to respond. In environments governed by real-time financial settlement, that elasticity disappears.

Collateral movements can be triggered within minutes. Margin enforcement may be automated through smart contracts. If sufficient funding is not present at the precise moment of settlement, the trade fails. BIS simulations in recent wholesale CBDC experiments suggest that intraday liquidity volatility rises meaningfully under real-time frameworks. Funding requirements become more variable within shorter windows. Institutions must either maintain larger idle buffers or develop dynamic collateral mobility systems capable of near-continuous adjustment. The key structural change is psychological as well as operational. Funding is no longer a daily exercise. It becomes a continuous state.

4. Netting Windows under Pressure

Netting historically reduced systemic fragility. Clearinghouses aggregated positions so that only net exposures settled. This reduced the gross funding required at any given moment. In many tokenized environments, gross settlement logic dominates. Even where netting layers are being developed, they often operate differently from traditional CCP structures.

When transactions settle atomically on a per-trade basis, liquidity demands increase. Offset positions may not be aggregated before settlement. The same balance sheet must support each transaction independently unless explicit netting logic is encoded into the system. This does not necessarily increase credit duration risk, but it can amplify liquidity volatility. The result is subtle but important. A portfolio that appears balanced in aggregate may experience momentary funding stress if multiple transactions finalize simultaneously. For allocators evaluating managers or engaging with a digital asset management company, this is not an abstract systems discussion. It determines how capital must be structured during volatility spikes.

5. Continuous Markets and the End of “After Hours”

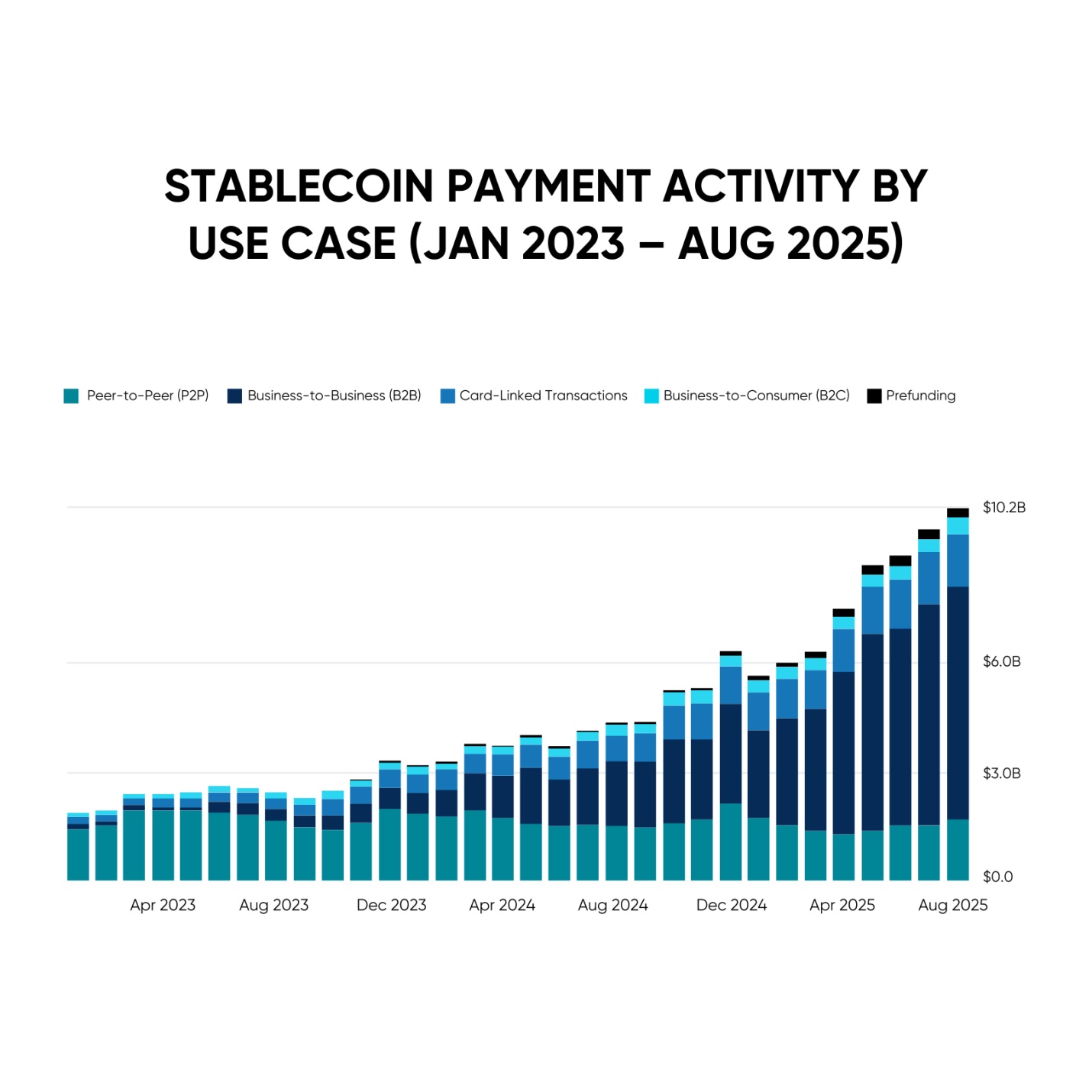

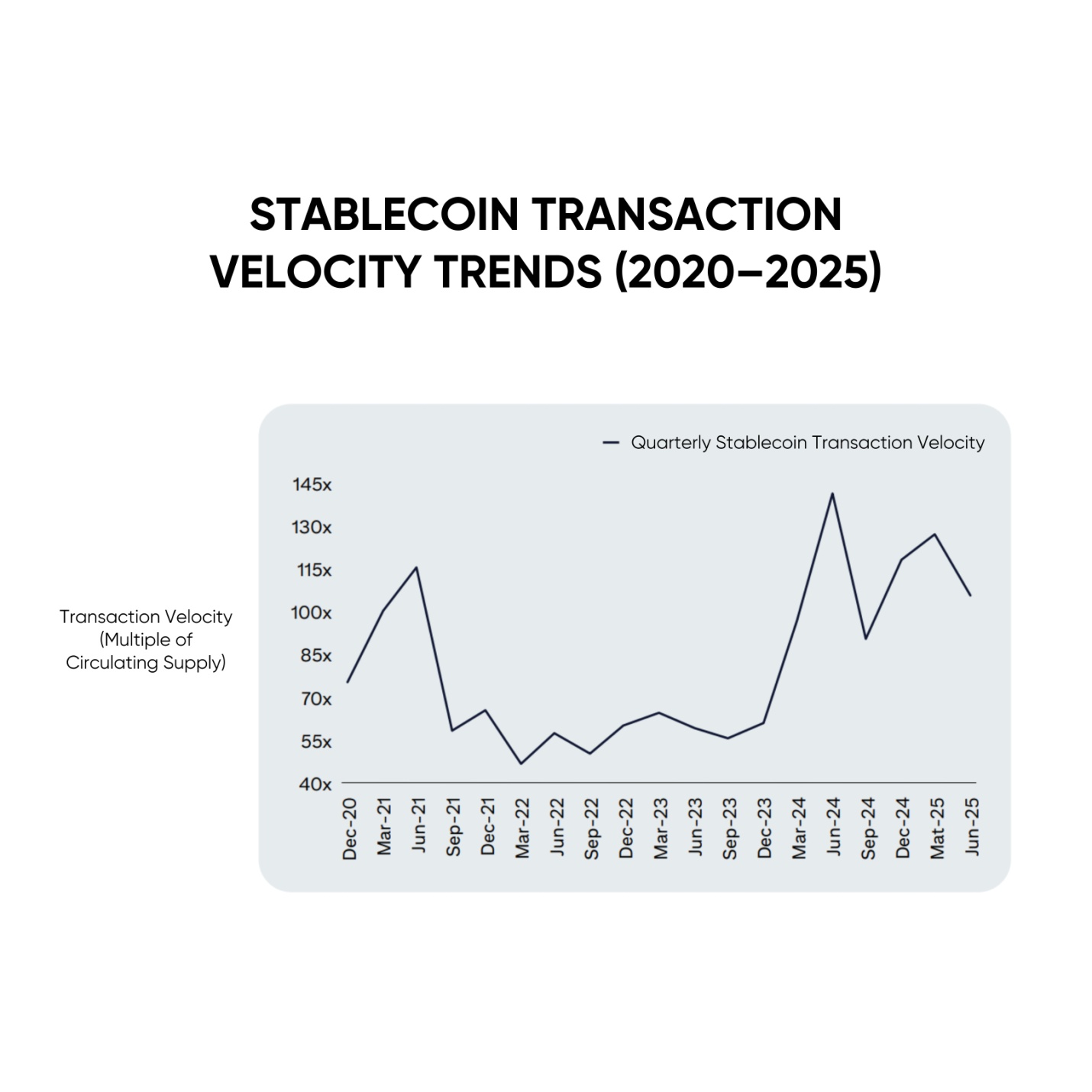

Blockchain-based systems operate without regard to traditional market hours. Stablecoin supply exceeded $130 billion in 2025, with meaningful settlement activity occurring outside U.S. trading windows. Tokenized repo and collateral mobility pilots operate around the clock. Liquidity events can now occur at 2:00 AM on a Sunday. This has implications beyond convenience. Treasury operations, collateral oversight, and monitoring functions must adapt to continuous exposure. Firms that rely on daily funding cycles or human-driven reconciliation processes face structural vulnerability. The New Risk Clock does not pause overnight.

Managers offering digital asset management services or providing blockchain and digital asset consulting must account for this continuity explicitly. Infrastructure readiness becomes inseparable from capital discipline.

6. Credit Risk Reframed

One might assume that faster settlement reduces risk. In one dimension, it does. Shorter exposure windows mean counterparty obligations are resolved more quickly. Bilateral credit duration shrinks. However, funding pressure intensifies. In decentralized environments, automated liquidation engines enforce collateral thresholds immediately. During volatility events, forced liquidations can cascade within minutes. We have observed this dynamic repeatedly in DeFi markets.

For institutions exploring navigating DeFi finance assets with consultants, the lesson is consistent. Yield amplification strategies become fragile when collateral calls are instantaneous. Liquidity becomes the dominant risk variable. Duration risk decreases. Liquidity fragility increases.

7. Operational Risk Without Buffers

Traditional systems assumed that operational breaks could be corrected before final settlement. Under compressed cycles, error correction windows narrow dramatically. A misrouted transfer, a compliance flag, or a smart contract misconfiguration does not produce a delay. It produces an immediate failure. Industry surveys conducted across tokenized asset pilots in 2024 and 2025 consistently ranked operational readiness above regulatory uncertainty as the primary adoption constraint.

This aligns with what we observe when institutions begin evaluating digital asset consulting firms with boutique providers. The core question is not performance optimization. It is resilience at settlement speed. The absence of temporal buffers demands precision.

8. Tokenized Collateral and Funding Sensitivity

Tokenized securities and programmable cash enable near-instant settlement of repo, treasury transfers, and structured products. This reduces reconciliation friction and can lower counterparty duration exposure. At the same time, it requires pre-funding discipline.

Real-time valuation and automated margin enforcement create intraday recalibration pressure. Treasury teams must monitor exposures continuously rather than relying on batch reporting. For allocators considering long-term investment in digital assets, understanding whether a manager maintains conservative liquidity buffers becomes critical. Speed does not substitute for stability.

9. Portfolio Construction Under Compression

Settlement compression affects how exposure should be evaluated across digital asset investments.

Networks with deeper liquidity and more robust settlement infrastructure tend to absorb volatility more effectively. This distinction becomes relevant when comparing altcoins vs. major cryptocurrencies. Smaller tokens often experience sharper funding stress during high volatility, particularly when collateral mobility is limited.

The difference is structural rather than narrative-driven. When markets compress, thin liquidity and weak infrastructure amplify instability. Allocators seeking transparent investment solutions should assess not only asset selection but also the operational framework supporting settlement.

The Kenson Perspective

Settlement compression is frequently framed as pure efficiency. Faster rails are portrayed as inherently safer. We do not view the shift so simply. From our perspective, accelerated settlement removes time as a risk buffer. While duration risk declines, liquidity volatility increases. Operational precision becomes non-negotiable. Funding assumptions must be conservative rather than optimized.

In environments governed by real-time financial settlement, discipline must scale with speed. Our framework prioritizes liquidity durability, infrastructure resilience, and conservative collateral positioning. We are less concerned with maximizing throughput than with ensuring survivability under stress. Speed without structure magnifies fragility. The New Risk Clock does not forgive miscalculation.

Looking Ahead

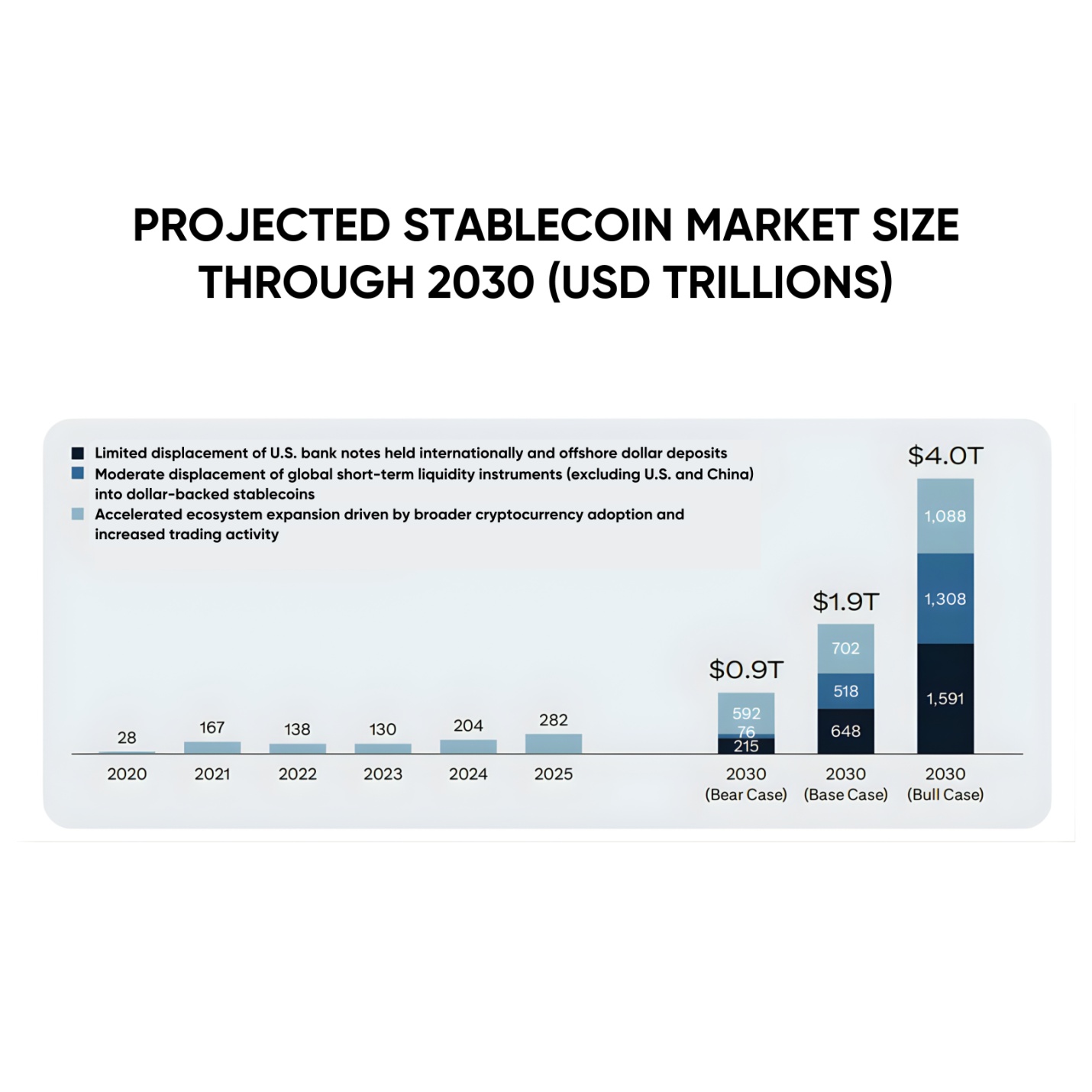

Industry momentum toward tokenized settlement infrastructure is accelerating. Cross-border CBDC pilots, tokenized government bonds, and programmable repo networks are expanding. Multi-trillion-dollar projections for tokenized markets by the end of the decade reflect structural adoption, not experimental novelty. Settlement compression will intensify.

The critical question for allocators is not whether to participate in evolving digital infrastructure. It is whether exposure is governed by managers who understand that compressed time changes

Part II: Rebuilding Risk Models for Minute-Based Exposure

If settlement compression changes when exposure becomes real, the next question is unavoidable: how should risk be modeled when exposure crystallizes in minutes rather than days? Traditional stress testing frameworks were designed for slower clocks. Value-at-risk models assumed daily price intervals. Liquidity stress models operated on end-of-day collateral snapshots. Margin simulations were often calibrated around overnight funding assumptions. Those inputs no longer reflect the lived reality of markets migrating toward real-time financial settlement.

The transition is not cosmetic. It alters the geometry of risk.

1. From End-of-Day to Intraday Stress

Historically, a firm’s exposure profile could be reviewed at the close of business. Treasury teams evaluated funding sufficiency after markets settled. Margin calls were processed in structured cycles. Even in volatile periods, exposure accumulated gradually across trading hours. Under compressed cycles, exposure can accumulate and finalize within a single hour. Stress models now require intraday simulation capability. Institutions operating on tokenized rails must estimate not only daily price shocks but also minute-level liquidity clustering. When multiple counterparties settle simultaneously, funding pressure can spike sharply even if net positions remain modest.

Recent industry pilots in tokenized repo and wholesale CBDC environments indicate that intraday liquidity volatility can exceed traditional models by meaningful margins. While credit duration declines, funding variability increases. The critical failure mode is not insolvency. It is temporary illiquidity at the wrong moment. For allocators evaluating a digital asset management company, the distinction matters. A manager may hold fundamentally sound positions and still experience stress if liquidity planning lags settlement speed.

2. The Collapse of Sequential Risk

In traditional markets, risks unfolded sequentially. Price risk materialized first. Margin calls followed. Liquidity adjustments came afterward. The process was layered. In compressed environments, risks collapse into simultaneity. Price movement, collateral revaluation, margin enforcement, and settlement finality can occur within the same time window. There is no structured separation. This simultaneity increases operational sensitivity. Smart contracts governing margin logic execute automatically. Automated liquidation engines in decentralized venues respond deterministically. Human discretion plays a reduced role.

Institutions engaging in digital asset management consulting services increasingly focus on whether internal systems can monitor and respond at the cadence of automated rails. The question is no longer whether exposure exists. It is whether response speed matches settlement speed.

3. Liquidity Engineering in a Continuous Market

Continuous markets introduce a new discipline: liquidity engineering. Traditional treasury operations optimized funding against known market hours. Repo markets, central bank facilities, and payment systems operated within business-day constraints. Digital infrastructure operates continuously. Stablecoins settle at all hours. Tokenized collateral moves without regard to timezone. This requires a redesign of liquidity buffers.

Conservative positioning now means maintaining reserves capable of absorbing intraday clustering without forced asset sales. It also requires diversified funding channels. Reliance on a single liquidity venue increases vulnerability under compression. Managers offering digital asset management services or presenting themselves as a crypto asset management provider must demonstrate that liquidity planning extends beyond yield capture. Liquidity durability is not a secondary metric. It becomes central to capital protection.

4. Credit Risk Shortens, Funding Risk Expands

It is tempting to conclude that atomic settlement reduces systemic risk. In certain respects, that is accurate. Counterparty duration risk declines when trades finalize instantly. Bilateral exposure windows shrink. However, funding risk expands. Under compressed settlement conditions, capital must be available precisely when obligations arise.

There is no buffer for delayed transfer. Institutions without real-time liquidity visibility risk settlement failure even if their balance sheet appears strong in aggregate. This dynamic is visible in decentralized finance, where liquidation cascades occur when collateral values fall below thresholds. Automated enforcement accelerates stress. For investors evaluating navigating the digital asset market, the structural lesson is clear. Stability depends less on directional accuracy and more on funding resilience.

5. The Role of Stablecoins and Tokenized Cash

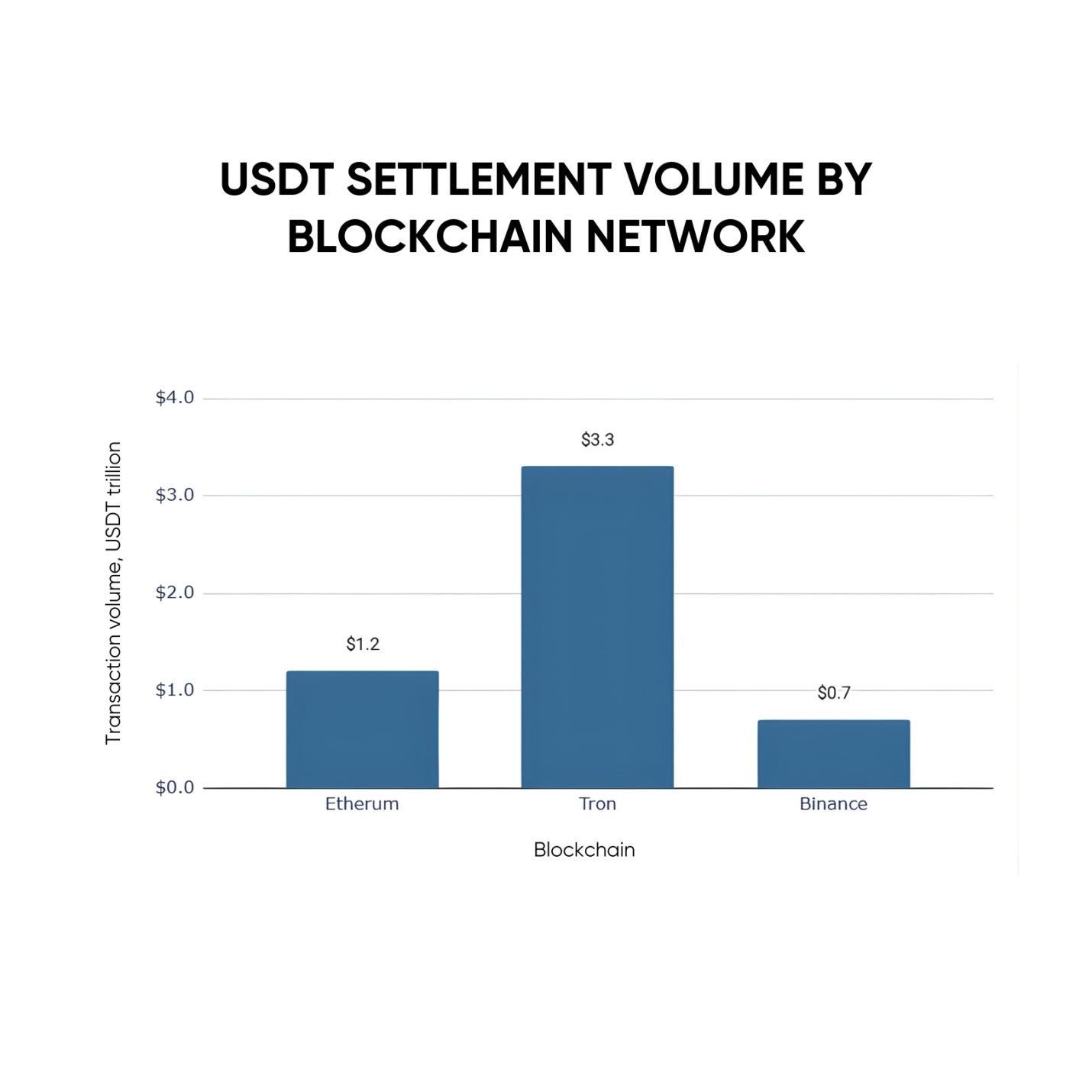

Stablecoins have become central to real-time settlement architecture. With circulating supply exceeding $130 billion in 2025, stablecoins function as programmable cash across exchanges, lending venues, and tokenized securities platforms. However, reliance on stablecoins introduces concentration and redemption risk. Reserve transparency, governance quality, and liquidity backing must be evaluated carefully. During stress events, confidence in convertibility becomes critical.

Institutions seeking stablecoins for investment exposure or integrating stablecoin rails into digital asset investment solutions must examine not only yield opportunities but also reserve composition and redemption mechanics. Settlement compression amplifies redemption sensitivity. A confidence shock can propagate rapidly when settlement finality is instantaneous.

6. Recalibrating Portfolio Construction

Compressed settlement reshapes portfolio construction in subtle ways. Asset liquidity profiles matter more under minute-based settlement than under T+2 cycles. Assets that appear tradable under normal conditions may become illiquid when collateral must be mobilized instantly. This distinction becomes evident when comparing altcoin investment options to exposure in deeper markets. Major networks often exhibit greater liquidity resilience. Smaller tokens may face sharper price gaps under stress, particularly when leveraged positions unwind simultaneously.

Investors evaluating long-term investment in digital assets should therefore assess liquidity stratification within portfolios. Concentration in thin markets increases settlement fragility. Portfolio managers must integrate liquidity tiering into allocation frameworks. Exposure size must reflect exit capacity under compressed conditions.

7. Infrastructure Risk and Interoperability

As tokenized markets expand, interoperability between networks becomes increasingly important. Fragmented liquidity across chains can create settlement bottlenecks. Cross-chain bridges, while enabling transfer, introduce smart contract risk and security vulnerabilities.

Industry initiatives such as the Canton Network consortium and BIS-led interoperability pilots aim to standardize messaging and settlement frameworks. Yet fragmentation persists. Institutions engaging in blockchain asset consulting must evaluate interoperability risk alongside asset risk. A settlement failure on one network can disrupt collateral flows elsewhere. Settlement compression increases the cost of fragmentation.

8. Operational Governance in Compressed Environments

Operational governance must evolve alongside settlement speed. Traditional separation between front office, risk, and treasury functions may require tighter integration. Real-time dashboards, automated alerts, and pre-programmed contingency protocols become necessary. Firms positioning themselves as leading digital asset consulting specialists increasingly emphasize governance architecture. Policies must define liquidity thresholds, collateral mobility triggers, and stress response procedures in advance.

Under compression, improvisation is costly. Institutions exploring partnerships with a digital asset strategy consulting firm should prioritize operational readiness over marketing sophistication.

9. DeFi, Automation, and Cascading Risk

Decentralized finance introduces unique considerations. Automated liquidation engines, algorithmic stablecoins, and on-chain leverage can amplify volatility. During prior stress events, DeFi markets demonstrated how quickly liquidations can cascade when collateral thresholds are breached. Under compressed settlement conditions, liquidation cycles can unfold within minutes, magnifying price dislocation.

For investors considering exposure through decentralized finance advisory, the lesson is discipline. Yield generation must be evaluated relative to liquidation risk under compressed timelines. In this context, risk management in crypto investments becomes less about directional speculation and more about structural vulnerability.

10. Institutional Adoption and Regulatory Trajectory

Regulatory bodies increasingly acknowledge settlement compression. The U.S. move toward T+1 equity settlement illustrates broader momentum toward faster cycles. Wholesale CBDC pilots across Europe and Asia emphasize real-time clearing.

These developments suggest that compressed settlement is not limited to digital-native markets. Traditional markets are converging toward faster rails. As this convergence accelerates, allocators must reassess how digital asset investments integrate with broader portfolios. Liquidity modeling across asset classes may require harmonization. Settlement compression is not a niche phenomenon. It is systemic evolution.

The Kenson Perspective

From our vantage point, settlement compression represents neither unqualified progress nor inherent danger. It represents a shift in where risk resides. Duration risk decreases. Liquidity risk intensifies. Operational precision becomes central.

We approach this environment conservatively. Liquidity buffers are treated as structural safeguards rather than idle capital inefficiencies. Exposure sizing reflects market depth. Infrastructure partners are evaluated for resilience rather than novelty. Our role is not to accelerate settlement for its own sake. It is to ensure that capital survives within accelerated systems. Speed without discipline magnifies fragility. Discipline aligned with speed enhances resilience.

Part III: Fund Structures, Allocator Implications, and Institutional Adaptation

If Part I examined the structural shift and Part II addressed the modeling response, the next layer is institutional architecture. Compressed settlement does not simply affect trading desks. It affects how funds are structured, administered, governed, and evaluated by capital allocators.

For high-net-worth investors and institutional allocators, the practical question is no longer whether digital markets are accelerating. It is whether the managers operating within them are structurally prepared for that acceleration.

1. Fund Structures Under Compressed Settlement

Traditional fund models evolved in environments where settlement lags provided operational elasticity. Subscription cycles, redemption windows, and NAV calculations were aligned with end-of-day clearing assumptions. Even hedge structures relied on clearinghouses and margin processes calibrated to daily cadence. In tokenized and blockchain-based markets, settlement compression introduces asymmetry between asset liquidity and investor liquidity.

Consider a digital asset management company operating within 24/7 markets. Under real-time financial settlement, portfolio assets may experience minute-level liquidity swings. However, investor capital inflows and outflows may still be governed by structured windows. This creates timing mismatches between internal funding obligations and external capital commitments.

Funds engaging in cryptocurrency fund administration must therefore re-evaluate reconciliation processes. NAV transparency, valuation timing, and redemption gates require recalibration. The role of a crypto fund administrator becomes more operationally intensive when settlement cycles compress.

Whereas traditional administration reconciled transactions within daily cycles, compressed environments demand near-continuous ledger verification and collateral tracking. Allocators evaluating a fund management company must now examine operational cadence as carefully as asset selection.

2. Portfolio Management in a Minute-Based System

Compressed settlement reshapes the function of digital asset portfolio management. Portfolio managers cannot rely on deferred funding assumptions when reallocating exposure. Capital must be available at the precise moment rebalancing occurs.

This changes how leverage is approached. In slower systems, modest leverage could be managed with predictable margin windows. Under compression, leverage amplifies funding sensitivity. Automated margin triggers can cascade rapidly when price shocks occur.

For investors assessing investment analysis and portfolio management processes within digital strategies, the key question becomes liquidity discipline. Does the manager maintain conservative leverage ratios? Are funding buffers sized for intraday volatility rather than daily averages?

The distinction matters more than marginal yield enhancement. Firms presenting themselves as a crypto investment firm may highlight performance narratives. A disciplined allocator should instead evaluate funding architecture. Settlement compression exposes structural weakness faster than market volatility alone.

3. The Evolution of Digital Fund Advisory

The acceleration of settlement has given rise to a new category of advisory demand. Institutions require guidance not only on asset exposure but also on operational alignment. This is where finance asset management consulting intersect with infrastructure strategy. A credible digital asset management consultant must understand both balance sheet risk and settlement architecture.

In practice, this has increased demand for digital asset management consulting services that address:

- Intraday liquidity modeling

• Collateral mobility frameworks

• Stablecoin concentration risk

• Interoperability resilience

• Automated margin governance

The firms that will endure are not those that simply promote innovative investment solutions. They are those that provide secure digital asset consulting solutions grounded in operational realism. Settlement compression has shifted consulting emphasis from asset discovery to structural resilience.

4. Venture and Growth Capital Under Compressed Rails

Settlement compression also affects venture and growth strategies. Firms involved in venture capital fund management increasingly allocate capital to tokenized infrastructure, DeFi protocols, and blockchain-based clearing platforms.

However, venture exposure layered onto compressed settlement rails introduces additional timing risk. Token unlock schedules, liquidity mining incentives, and protocol governance changes can interact with automated settlement logic unpredictably. Allocators evaluating cryptocurrency growth fund management or exposure to early-stage tokenized ecosystems must incorporate liquidity cliffs into risk assessment. Compressed cycles amplify volatility during unlock events. The absence of temporal buffers magnifies structural transitions.

5. Stablecoins, Liquidity Pools, and Systemic Sensitivity

Stablecoins are central to compressed settlement infrastructure. They function as programmable settlement cash across exchanges and tokenized securities platforms. Institutions exploring stablecoin investment consultant services must evaluate reserve transparency, redemption pathways, and issuer governance. Under compressed conditions, redemption stress can propagate rapidly.

If settlement finality is instantaneous, confidence shocks travel without friction. Liquidity pools within decentralized venues further complicate this dynamic. Automated market makers provide continuous liquidity but rely on algorithmic pricing. During sharp moves, slippage can widen significantly, increasing funding demands at precisely the moment liquidity is most needed. For allocators, the lesson is not avoidance. It is prudence. Settlement compression punishes complacency.

6. The Consulting Ecosystem in a Compressed Market

As compressed settlement becomes institutionalized, demand for structured advisory has expanded. Businesses seeking to integrate tokenized rails require guidance beyond technical deployment. This has accelerated interest in digital asset consulting services for businesses, particularly in areas such as treasury tokenization and programmable collateral.

However, not all advisory positioning is equal. Firms marketing themselves as leading digital asset consulting specialists must demonstrate governance depth rather than narrative fluency.

Institutions considering digital asset consulting for startups should distinguish between growth acceleration advice and structural resilience advice. Compressed settlement is unforgiving. Advisory credibility depends on whether liquidity discipline is embedded within strategy. When evaluating digital asset consulting firms, allocators should examine how those firms address:

- Liquidity stress testing

• Settlement clustering risk

• Operational fallback protocols

• Cross-chain transfer fragility

The difference between cosmetic advisory and durable advisory becomes visible under stress.

7. DeFi Integration and Institutional Guardrails

DeFi platforms introduce unique challenges within compressed systems. Automated liquidation engines, yield aggregation strategies, and tokenized collateral pools operate deterministically. Institutions engaging in DeFi finance consulting services must ensure governance overlays are layered onto protocol automation.

In practice, this means conservative exposure sizing, pre-defined liquidation thresholds, and limited reliance on recursive leverage. Compressed settlement reduces discretion windows. Once a threshold is breached, execution is automatic. For high-net-worth allocators seeking digital asset investments that incorporate DeFi exposure, understanding the mechanical nature of liquidation risk is essential. The system does not wait for committee approval.

8. Institutional Transparency and Trust

Compressed settlement also elevates the importance of transparency. When exposure materializes rapidly, investors demand real-time visibility. This is where transparent investment solutions become more than a marketing phrase. Continuous reporting, on-chain verification, and reconciliation dashboards provide assurance that liquidity buffers are intact.

Managers positioning as strategic digital asset consulting partners must recognize that trust is earned through operational clarity. Under compression, opacity becomes risk.

9. Comparing Traditional and Digital Management Models

Traditional managers often emphasize track record and macro positioning. Digital-native managers must emphasize liquidity architecture and funding discipline. A portfolio management consultant operating in tokenized markets cannot rely solely on performance analysis. They must incorporate settlement sensitivity modeling.

Similarly, firms presenting themselves as bitcoin investment consultants must demonstrate awareness of funding risk beyond directional exposure. Compressed settlement reframes risk hierarchy. Liquidity outranks yield.

10. Institutional Readiness Beyond 2025

The convergence between traditional and digital settlement infrastructure will accelerate. Equity markets have already moved to T+1. Wholesale CBDC pilots suggest further compression ahead. Tokenized bond issuance continues to expand. As these systems integrate, compressed settlement will not remain confined to digital-native markets. It will influence broader capital flows.

Allocators must therefore consider digital settlement risk not as a separate silo but as part of systemic evolution. Managers prepared for compressed cycles in digital assets may be better positioned as traditional markets accelerate.

The Kenson Perspective

From our perspective, settlement compression is not a race toward speed. It is a redefinition of responsibility. Managers operating within accelerated systems must treat liquidity as structural capital. We approach exposure with the assumption that funding demands can cluster unpredictably. Liquidity buffers are not idle inefficiencies. They are resilience instruments. We do not rely on overnight adjustments. We design for intraday stress.

As a firm focused on disciplined capital stewardship, we evaluate infrastructure durability, stablecoin concentration, interoperability risk, and operational readiness before emphasizing yield narratives. Compressed settlement rewards preparation and punishes overextension. Our role is not to chase acceleration. It is to ensure capital remains intact within accelerated systems.

Part IV: Allocator Decision Frameworks in an Accelerated Market

The acceleration of settlement is no longer a technical discussion reserved for infrastructure architects. It is a capital governance issue. As markets transition toward real-time financial settlement, allocators must recalibrate how they evaluate managers, strategies, and operational architecture. Speed changes what matters.

In slower systems, allocators focused heavily on directional thesis, macro positioning, and relative performance. Liquidity planning was assumed. Operational resilience was often secondary.

Under compressed settlement conditions, that hierarchy reverses. Liquidity durability, collateral structure, and funding responsiveness become foundational.

1. What Allocators Must Now Ask

When assessing exposure to digital markets, allocators should evaluate not only asset selection but settlement sensitivity.

The questions become more structural:

- How does the manager model intraday liquidity clustering?

- What proportion of portfolio capital is held in immediately mobilizable form?

- Are stablecoin exposures diversified and redemption-tested?

- Does the manager rely on thin DeFi liquidity pools for yield enhancement?

- Is leverage sized relative to minute-based margin triggers rather than daily averages?

These are not cosmetic due diligence points. They determine survivability under compression. Settlement compression reveals fragility quickly.

2. Differentiating Strategy from Structure

In an accelerated environment, strategy and structure cannot be separated. A high-yield opportunity embedded within fragile liquidity rails carries asymmetric risk. Conversely, moderate yield within deep and transparent infrastructure may provide more durable outcomes.

This distinction becomes particularly relevant in conversations about cryptocurrency investment strategies. Yield optimization frameworks that rely on recursive leverage or thin liquidity provisioning are structurally sensitive to compressed settlement cycles. Investors evaluating digital asset investment solutions must therefore distinguish between headline return narratives and funding integrity. The difference between a prudent manager and an opportunistic one is often visible in liquidity ratios rather than token selection.

3. Major Networks vs. Peripheral Markets

Earlier we referenced the structural difference between altcoins vs. major cryptocurrencies. Under compressed settlement conditions, this difference widens. Major networks benefit from deeper liquidity pools, broader collateral acceptance, and more mature custody infrastructure. Peripheral tokens may experience disproportionate price gaps and funding stress when volatility rises.

This does not invalidate selective exposure to emerging assets. However, exposure sizing must reflect liquidity depth. Capital allocated to thin markets should assume elevated settlement sensitivity. Investors exploring altcoin investment options must incorporate liquidity stratification into portfolio construction. Under compression, liquidity fragility surfaces rapidly.

4. Bitcoin, Stability, and Institutional Preference

Institutional flows continue to favor Bitcoin and Ethereum as foundational exposure. This is not merely a narrative preference. It reflects infrastructure maturity. Managers positioning as bitcoin fund manager entities or offering guidance through bitcoin investment advice frameworks must recognize that liquidity depth and settlement reliability drive institutional comfort.

Similarly, investors seeking stablecoins for investment exposure should prioritize reserve transparency and issuer governance over incremental yield differentials. In compressed systems, confidence in convertibility is foundational.

5. The Role of Index and Growth Vehicles

Index-style exposure, including strategies aligned with cryptocurrency index fund management, may offer structural simplicity relative to highly leveraged yield strategies. Diversification across major networks can mitigate liquidity concentration risk.

By contrast, aggressive vehicles within cryptocurrency growth fund management may face sharper settlement sensitivity during volatility spikes, particularly when capital flows cluster. Allocators must therefore calibrate exposure not only by expected return but by settlement geometry. Acceleration penalizes excess leverage and illiquid concentration.

6. Fund Administration and Governance Integrity

As settlement cycles compress, administrative integrity becomes critical. Accurate real-time reconciliation, transparent custody reporting, and independent oversight are essential. Firms offering fund management services in digital markets must ensure that internal systems match settlement cadence. Delayed reconciliation in a minute-based market creates blind spots. Allocators should examine whether managers maintain robust internal controls rather than relying solely on external marketing narratives. Operational readiness is not optional under compression.

7. The Consulting Landscape: Substance vs. Branding

The expansion of advisory demand has produced a crowded landscape of firms presenting themselves as a global digital asset consulting firm. However, compressed settlement distinguishes substance from surface positioning.

A credible digital asset strategy consulting firm will address liquidity engineering, collateral pathways, interoperability fragility, and governance architecture. Superficial advisory that focuses solely on growth potential or token narratives fails to address the structural core of accelerated markets.

Institutions engaging in digital asset consulting for compliance must also understand that compliance frameworks must operate at settlement speed. Delayed review processes cannot prevent automated liquidations or margin triggers.

Compressed cycles require integrated governance.

8. DeFi Participation with Guardrails

DeFi remains a source of innovation and yield experimentation. However, automated enforcement mechanisms intensify risk during volatility. Allocators working with a stablecoin investment consultant or exploring exposure through consultancy for DeFi finance investments should insist on conservative leverage limits and pre-defined exit protocols.

The critical principle is simple. In automated systems, discipline must be coded in advance. Settlement compression does not allow committee deliberation after thresholds are breached.

9. Long-Term Allocation in the Digital Age

The structural evolution toward faster settlement aligns with broader digitization trends. Markets are unlikely to revert to slower cycles. Institutional infrastructure is adapting. For allocators committed to long-term investment in digital assets, the focus must shift from tactical timing to structural durability. This includes evaluating infrastructure resilience, meaning whether the underlying blockchain networks, custodians, and settlement rails can withstand congestion, validator outages, or sudden spikes in transaction demand without impairing execution or collateral mobility.

It requires deliberate liquidity tiering within portfolios, where assets are classified not only by return profile but by mobilization speed, depth of secondary markets, and expected slippage under stress. Liquidity assumptions must be based on adverse conditions, not normal trading environments. It involves careful assessment of stablecoin counterparty risk, including issuer reserve transparency, redemption mechanics, jurisdictional exposure, governance controls, and the concentration of market share across dominant issuers. It demands operational integration across custody providers, ensuring seamless asset transfer, reconciliation accuracy, and real-time visibility across wallets, exchanges, and settlement venues without introducing transfer delays or coordination gaps.

Finally, it requires stress testing under minute-based volatility scenarios, modeling clustered margin calls, simultaneous collateral movements, and short-duration liquidity shocks rather than relying solely on daily or end-of-day risk frameworks.

These considerations define sustainable participation in accelerated systems.

10. Risk Hierarchy under Compression

When settlement cycles compress, the hierarchy of risk shifts. Liquidity risk rises above directional risk. In compressed settlement environments, capital failure is more likely to stem from funding shortfalls than incorrect market views. A portfolio can be directionally sound and still experience stress if collateral cannot be mobilized at the precise moment required. Operational precision becomes central. Automated margin enforcement, atomic trade settlement, and continuous ledger updates leave little tolerance for execution error. Systems, controls, and monitoring frameworks must operate at the same cadence as settlement infrastructure.

Funding concentration outweighs marginal yield advantage. Exposure that depends on a narrow set of liquidity venues, stablecoin issuers, or counterparties may deliver incremental return in calm conditions but introduces asymmetric vulnerability during stress events. Governance clarity outweighs marketing fluency. In accelerated markets, durable performance depends less on narrative positioning and more on clearly defined risk thresholds, pre-established response protocols, and disciplined exposure sizing under volatile conditions.

This reordering requires allocators to reassess traditional evaluation criteria. A firm that emphasizes aggressive return targets without detailing funding safeguards is misaligned with compressed market reality. By contrast, a manager that prioritizes liquidity buffers and conservative leverage may appear restrained during bull markets but is structurally positioned for durability.

The Kenson Perspective

We view settlement compression as a structural inevitability. Technology will continue to accelerate clearing, collateral movement, and funding cycles. Tokenized securities, programmable cash, and automated enforcement systems will expand. Our responsibility is not to accelerate with them blindly. It is to align capital exposure with structural resilience.

We approach liquidity as a core asset. We prioritize infrastructure maturity over novelty. We limit leverage relative to minute-based margin sensitivity. We evaluate stablecoin concentration and counterparty exposure conservatively. In accelerated systems, patience is not inertia. It is risk management. Compressed settlement does not reward speed alone. It rewards preparation.

Final Reflections: The New Risk Clock

The transition from T+2 to atomic settlement is more than a technical upgrade. It represents a redefinition of when exposure becomes real. Under compressed settlement risk, time is no longer a buffer. It is a constraint. Markets that once allowed for sequential adjustment now enforce simultaneous resolution. Funding, collateral, valuation, and execution converge. For allocators, the question is not whether to participate in accelerated digital markets. It is whether participation is governed by managers who understand the implications of compressed time.

As digital infrastructure integrates with traditional markets, settlement compression will influence broader capital flows. Those prepared for minute-based exposure will adapt more smoothly than those relying on outdated models. Acceleration is not inherently destabilizing. Misalignment between speed and governance is.

Discipline in an Accelerated Market

As digital infrastructure reshapes global finance, allocators must evaluate more than opportunity. They must evaluate resilience. Kenson Investments operates with a capital preservation lens within accelerated systems. Our focus remains liquidity durability, operational precision, and disciplined exposure management. If you are assessing digital strategies in a market defined by compressed settlement risk and real-time financial settlement, we invite you to explore how we approach structural resilience from an educational perspective. Learn how Kenson Investments frames risk in the digital age and how disciplined governance defines durable participation. Get in touch with our digital asset specialists.